As we look back at the first quarter of 2026 for the technology industry, AI has moved on from a test phase to mass deployment.

Even though the news of layoffs and automation from AI has captured our attention, the Q1 2026 Technology Trends we captured include several nuances around capital allocation, Agentic ROI gap, energy shortage, transformation of entry-level jobs and EU-based compliance offering the regulatory balance to AI’s unchallenged march.

TL;DR (At a Glance)

- Capital structure under scrutiny: For the first time, software companies have splurged at a scale we haven't witnessed since the 2001 Dot-Com Bubble. The 2026 capex guidance reached $660 to $690 billion, 35% above 2025 levels where 75% were contributed by investments into AI. Nvidia, OpenAI, Oracle, and CoreWeave commitments have passed $800 billion and OpenAI has projected a $14 billion loss for 2026 [2][3][4][5].

- The Agentic ROI gap: Even though Gartner reports that 80% of enterprise apps shipped or updated in Q1 embedded at least one agent, only 31% of organizations have pushed their agents from pilot to production and roughly 95% of GenAI pilot projects failed to generate any ROI [7][8].

- Custom ASIC vs. GPU: Custom Application-Specific Integrated Circuit (ASIC) shipments are projected to grow 44.6% in 2026 versus 16.1% for merchant GPUs, as Tech giants diversify their dependence on NVIDIA; Broadcom posted $8.4 billion in Q1 AI revenue, up 106% year over year [10][11].

- Power becomes the bill: Q1 wholesale power on the PJM grid rose 76% year over year, US residential rates hit 17.45 cents per kWh (+9.5%), and interconnection waits stretched to about 54 months [12][13][14].

- Open weights collapse cost: DeepSeek V4 and Qwen 3.5 reached near-frontier benchmarks at roughly one-twentieth the price of closed models; open share rose from 1% to 15% of the global market in twelve months [15].

- Entry-level erosion: Disclosed AI-attributed layoffs were 55,000 in 2025 (modeled displacement of 200,000 to 300,000), with junior finance, consulting, and software roles most exposed and firms cutting in anticipation [18][19].

- The compliance cliff: EU AI Act high-risk obligations were set for August 2, 2026 before a May 2026 political agreement to delay key parts, turning AI governance into a board-level operating cost [16][17].

Key Data for Q1 2026

| Key data | Technology Industry Q1 2026 |

|---|---|

| Hyperscaler capex (2026) | $660 to $690 billion guidance across the Big Five, about 36% above 2025, with roughly 75% tied to AI infrastructure [2][3][4] |

| Circular financing | Interlocking Nvidia, OpenAI, Oracle, and CoreWeave commitments exceed $800 billion; OpenAI projects a $14 billion loss for 2026 [5] |

| Agent embedding | 80% of enterprise apps shipped or updated in Q1 contain at least one agent, yet only about 31% of organizations run one in production [7] |

| Custom silicon | Custom ASIC shipments grow 44.6% in 2026 against 16.1% for merchant GPUs; Broadcom Q1 AI revenue up 106% year over year [10][11] |

| Grid pressure | Q1 wholesale power on the PJM grid rose 76% year over year; US residential rates reached 17.45 cents per kWh, up 9.5% [12][13] |

| Open-weight share | Open models moved from 1% to 15% of the global market in twelve months, at roughly one-twentieth the price of closed frontier models [15] |

| Labor | Disclosed AI-attributed layoffs were 55,000 in 2025, with AI models displacing 200,000 to 300,000 jobs [18] |

| Regulation | EU AI Act high-risk obligations were scheduled for August 2, 2026 before a May 2026 political agreement to delay key parts [16][17] |

Key Observations

Capital intensity, the ratio of Total Assets (or Total Capex) to Total Revenue at the largest platforms reached 45 to 57 percent while supply constraints slowed down the outlook for 2026.[2][3]. At the same time, the cost of inference fell sharply as open-weight models reached near-frontier quality.

Organizations now have a 2-tier AI model – open-weight for routine tasks and frontier models for complex inferences similar to what an expert human offers[15].

Enterprises embedded agents at scale but could book ROI in a minority of cases.

Regulators moved AI governance from policy to operating requirement, although the pressure from the US government on EU has slowed down the enforcement of Annex III use cases in employment, education, credit scoring, biometric identification, and critical infrastructure.

The physical grid began passing AI's power demand directly to consumers and voters [7][12][16], who has not responded kindly with protests building up across rural American communities were the majority of planned AI infrastructure are set to be build.

Skills in Demand

| Job function | Skill set |

|---|---|

| Technologist / Architect | Design for portability across GPU and custom ASIC, switching and verifying outputs from open and frontier models, and building governance (logging, human oversight) into agent architecture from the start. |

| Finance / Strategy | Read hyperscaler capex disclosures, model data-center IRR against 18-month hardware cycles, and assess counterparty and circular-financing concentration. |

| Consulting / Transformation | Develop scope documents for agent portfolios, separate ROI-positive workflows from stalled pilots, and lead the data and change-management work that the production requires. |

| Policy / Sustainability | Navigate interconnection queues, power-purchase agreements, EU AI Act conformity, and ISO 42001 governance. |

| General Management | Manage AI unit economics (cost per feature), FinOps discipline, and reskilling paths as junior knowledge work becomes obsolete. |

We observed seven trends shaping the quarter.

Contents

- Key Data for Q1 2026

- Key Observations

- Skills in Demand

- Trend 1: The AI Capital-Structure Shift, Circular Financing Meets the Capex Wall

- Trend 2: The Agentic ROI Gap

- Trend 3: The Silicon Boom

- Trend 4: The Power-and-Cost Squeeze, Grid Backlash Meets FinOps 2.0

- Trend 5: The Open-Weight Cost Collapse and Sovereign-AI Geopolitics

- Trend 6: The Entry-Level Erosion and the Reshaping of Post-MBA Finance and Consulting Roles

- Trend 7: The Compliance Cliff, EU AI Act Meets Agentic Deployment

- Key Takeaways

Trend 1: The AI Capital-Structure Shift, Circular Financing Meets the Capex Wall

The infrastructure spending hype that began in Q4 2025 went into overdrive in Q1 2026, when the combined 2026 capex guidance for the Big Five (Microsoft, Alphabet, Amazon, Meta, and Oracle) reached $660 to $690 billion, about 36% above the prior year, with close to 75% (around $450 billion) directed at AI servers, GPUs, and data centers [2][3].

Amazon guided to roughly $200 billion, Alphabet to $175 to $185 billion, Meta to $115 to $135 billion, Microsoft past $120 billion, and Oracle toward $50 billion, and every one of them described its market as supply-constrained rather than demand-constrained [3].

Capital intensity at 2001 Levels

Capital intensity at the largest platforms reached 45 to 57 percent of revenue, a level previously unthinkable for software businesses [2]. Investors were worried when they realized that the aggregate capex now exceeds internal cash generation. But each stock market correction was quickly picked up by institutional investors and sovereign funds that have the long-term time horizon to take on risks on such a large scale. Even the fundraising from stock markets was not enough as hyperscalers raised about $108 billion in debt during 2025, with projections of roughly $1.5 trillion in issuance over the coming years [4]. The most affected asset class was corporate bond, with AI-linked debt becoming the primary ROI factor for these indices.

How Sustainable are Circular-financing in AI

The circular financing, where vendors, AI model creators, Integrators, and Chip Manufacturers all purchased each other’s products to keep the cashflow story going, reached a new high when Nvidia committed up to $100 billion to OpenAI, and OpenAI builds data centers that can hold as many as 50,000 Nvidia GB200 chips each. Oracle Cloud infrastructure is powering the Flagship site in Texas, and CoreWeave, a buy and rent AI infrastructure company, all have interlocking agreements that exceeded $800 billion [5].

INSEAD researchers note the structures resemble the vendor-financing of the late dotcom era, while supporters call it a virtuous circle that locks in scarce supply [6][5].

The true stress test is monetization.

Investment versus monetization: who is catching up

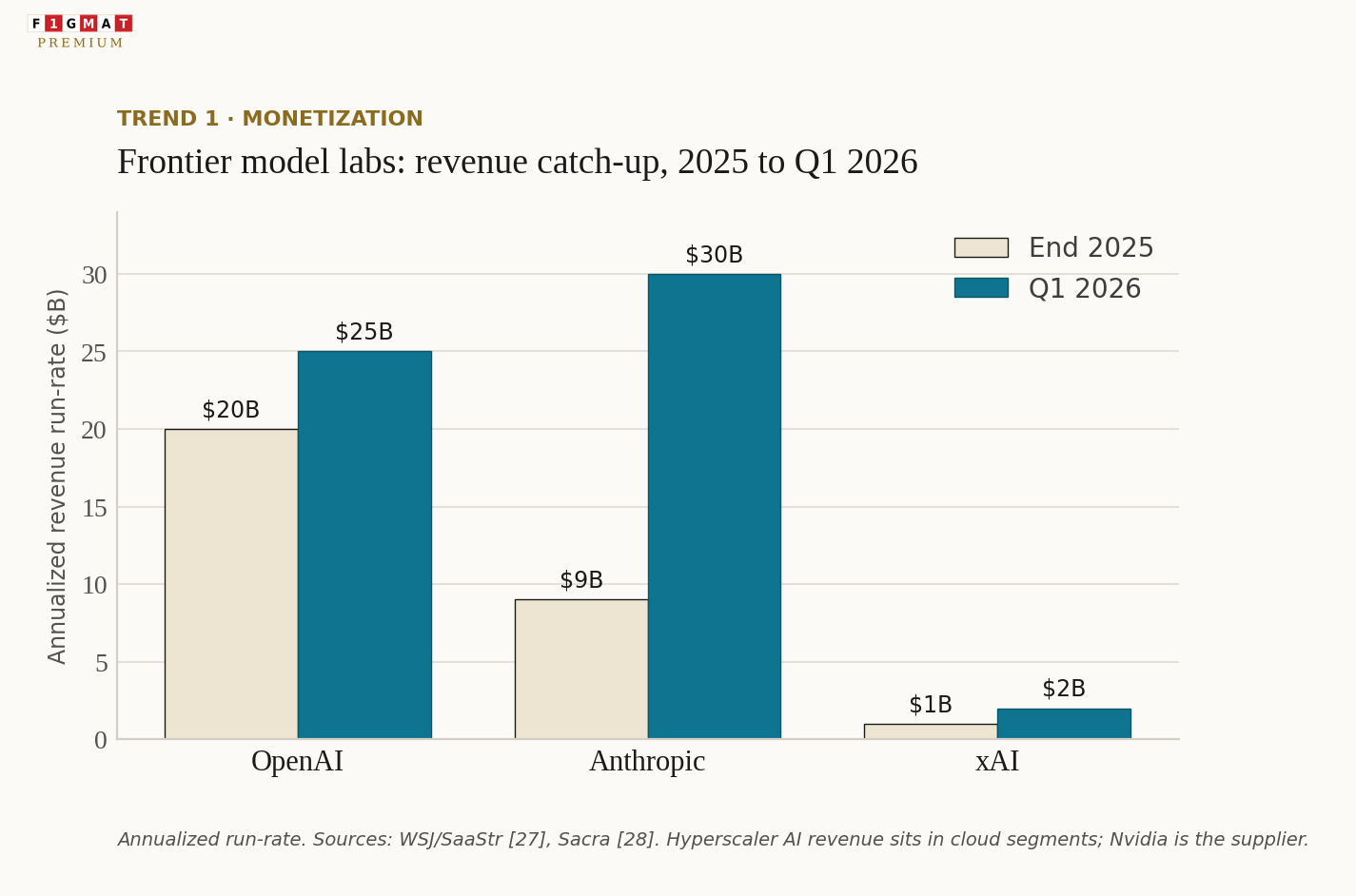

OpenAI ended 2025 near $20 billion in annual recurring revenue but still projects a $14 billion loss for 2026, and by Q1, investors started losing patience and began demanding split up of revenue outside these inflated vendor-funded growth [5].

Anthropic's annualized run-rate jumped from $9 billion at the end of 2025 to roughly $30 billion by Q1 2026, overtaking OpenAI's roughly $25 billion, with about 80% of Anthropic's revenue from enterprise customers and more than 1,000 accounts each spending over $1 million a year [27][28]. The question is whether the ARR will hold by the end of 2026 or compound faster than the capital being consumed to produce the value creation.

For the labs, the useful ratio is annualized revenue against cumulative capital raised or committed.

| Lab | Period | Annualized revenue (run-rate) | Cumulative capital raised/committed | Ratio (rev / capital) |

|---|---|---|---|---|

| OpenAI | End 2023 | $2B | $11B | 0.18 |

| End 2024 | $6B | $22B | 0.27 | |

| End 2025 | $20B | $60B | 0.33 | |

| Q1 / Apr 2026 | $24-25B | $170B+ | 0.14 | |

| Anthropic | End 2023 | $100M | $3B | 0.03 |

| End 2024 | $1B | $14B | 0.07 | |

| End 2025 | $9B | $42B | 0.21 | |

| Q1 / Apr 2026 | $30B | $72B | 0.42 | |

| xAI | End 2024 | $100M | $12B | 0.008 |

| End 2025 | <$1B | $20B+ | <0.05 | |

| 2026 | Small vs. capital | $20B+ (absorbed X) | lowest of group |

Before I go into the analysis, remember that the committed funds like OpenAI’s $100B commitment with Nvidia or the $500B Stargate commitment, versus cash actually spent, could mean different things.

If commitments are also calculated, OpenAI’s revenue-to-capital-raised ratio would look worse.

For Anthropic, the number adjustment is in how Anthropic reports cloud-reseller revenue on a gross basis, which inflates the top line relative to peers who publishes them as net.

Considering these two caveats, Anthropic’s Run Rate ( monthly revenue/quarterly revenue multiplied by 12 months, assuming the same market conditions will prevail) climbed steadily and, by April 2026, is the best of the three.

For a traditional Software company, the ratio of Revenue to Capital raised is above 1.0.

Below 1.0 means the lab has raised more than it earns in a year; above 1.0 means run-rate revenue exceeds all the money ever raised.

For any startups, especially AI labs with high capex, it is expected to be in the 40-50% range.

Anthropic’s surge was from the last quarter of 2025 to the first Quarter in 2026, where the lab caught up with OpenAI in Enterprise revenue, which jumped from $9B to $30B

The Burn Rate and Cash Flow positive projection, therefore, was favorable for Anthropic over OpenAI.

XAI was not a direct competitor.

Frontier model labs: revenue against capital

| Lab | Period | Annualized revenue (run-rate) | Cumulative capital raised/committed | Ratio (rev / capital) |

|---|---|---|---|---|

| OpenAI | End 2023 | $2B | $11B | 0.18 |

| End 2024 | $6B | $22B | 0.27 | |

| End 2025 | $20B | $60B | 0.33 | |

| Q1 / Apr 2026 | $24-25B | $170B+ | 0.14 | |

| Anthropic | End 2023 | $100M | $3B | 0.03 |

| End 2024 | $1B | $14B | 0.07 | |

| End 2025 | $9B | $42B | 0.21 | |

| Q1 / Apr 2026 | $30B | $72B | 0.42 | |

| xAI | End 2024 | $100M | $12B | 0.008 |

| End 2025 | <$1B | $20B+ | <0.05 | |

| 2026 | Small vs. capital | $20B+ (absorbed X) | lowest of group |

Capital and revenue figures are drawn from company disclosures and reporting collated by SaaStr [27], Sacra [28], and Software Thug [29]; valuations reflect funding rounds, not public market caps.

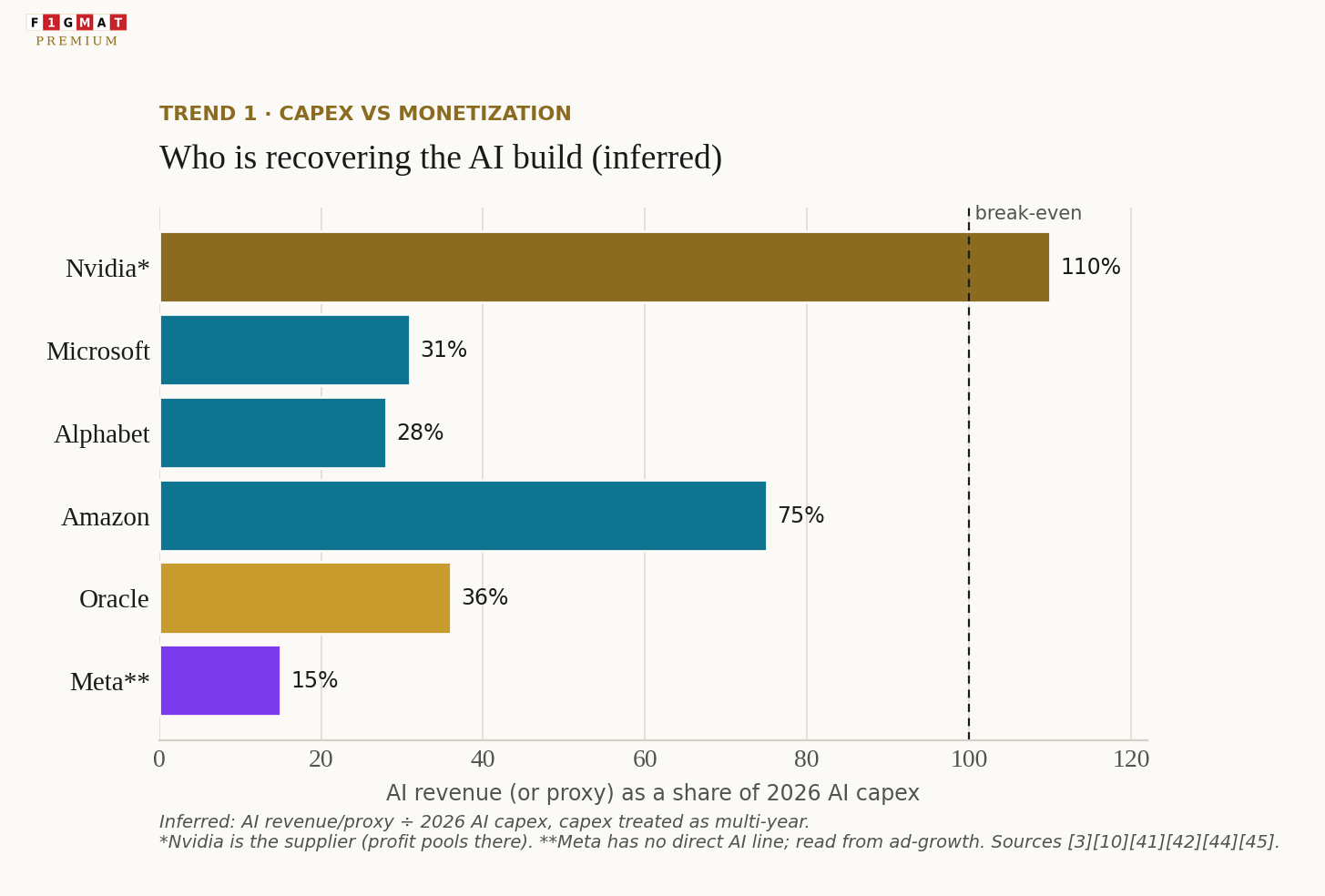

Hyperscalers: AI capex against AI revenue

| Company | 2026 AI/infra capex | AI revenue signal | Recovery picture (crunched) |

|---|---|---|---|

| Microsoft | $120B+ [3] | AI run-rate hit $37B, up 123% YoY; Azure up 39% [42] | AI revenue is roughly 31% of capex ($37B of $120B). At cloud gross margins (70%), that is $26B of gross profit, enough to cover about one year of AI-attributable depreciation. Closest of the group to breakeven on the build. |

| Amazon | $200B [3] | AWS at $37.6B/quarter ($150B run-rate, +28%); AI services run-rate above $15B; backlog $364B [44] | AWS throws off $57B/year of operating income at a 38% margin, which self-funds much of the build; AWS revenue is 75% of total capex. Strongest cash engine, though group free cash flow turns negative as the $200B capex starts. |

| Alphabet | $175B to $185B [3] | Google Cloud up 63% YoY; cloud backlog (RPO) $70B; Gemini serving cost cut 78% [43] | Cloud run-rate is $50B (RPO 1.4x revenue), about 28% of $180B capex; the 78% serving-cost cut is improving unit economics. AI-only recovery is lower because the capex also serves Search and YouTube. |

| Meta | $125B to $145B [41] | No direct AI line; AI lifts ad engagement and Advantage+ targeting, plus $2B WhatsApp paid-messaging run-rate [41] | Inferred: Q1 2026 revenue growth accelerated to 33% from the low-20s; attributing the step-up implies $15B to $25B of AI-linked ad revenue, 12% to 18% of the $135B capex. $85B+ operating income funds about two-thirds of capex; the rest from $81B cash and free cash flow. Capex is now 60% of revenue, up from 36% in 2025. |

| Oracle | $50B [3] | OCI up 54%/quarter, projected $18B for FY26; RPO backlog $455B, up 359% [45] | OCI revenue ($18B) is roughly a third of the calendar-2026 build, so free cash flow is negative and the spend is debt-funded. The $455B backlog (mostly already booked, forecast to reach $144B by FY30) is the bet that revenue catches up. |

| Nvidia | Modest vs revenue | The supplier: data-center revenue $200B+ run-rate at 75% gross margin; $41B returned to shareholders in FY26 [10] | Recovery exceeds 100%: roughly $150B of gross profit on minimal capex. |

For the hyperscalers, Microsoft and NVIDIA are two companies navigating the CAPEX vs. cashflow conundrum intelligently.

Even after a first movers advantage through collaboration with OpenAI, the two, like the rest of the Hyperscalers face a few risks:

a) Too Aggressive Infrastructure Build Out

Unlike traditional cloud infrastructure, which has a shelf life of over a decade, GPUs have a 3-4 year useful life. The degradation in AI server hasn’t deterred The Big Five from its planned acquisition of $2 trillion in AI assets [10] by 2030. Even if the annual depreciation is near $400 billion, a worst-case scenario is where the demand for their intelligence service drops while the hyperscalers are stuck with low-utility GPUs at the end of their shelf life.

b) Cash Flow Dynamics

It took decades of focused execution to reach a cash flow positive state for these Hyperscalers. For the first time, Capex inside these companies has exceeded their net cash flow. The giants are taking on more debt.

$108 billion in 2025, with projections toward $1.5 trillion over the next few years [46], is a sign of where these Tech giants are positioning themselves.

The most visible splurge was Amazon, whose free cash flow is expected to turn negative in 2026.

The impact is a constrained stock where buyback options are limited, and the sensitivity to changes in AI demand is high.

c) Category Benchmark

Traditionally, a capital intensity of 45 to 57% revenue is reserved and expected for utility companies.

When software companies show such a benchmark, the investor confidence will erode. Eventually, institutional investors will explore stocks with similar returns as software of the Saas era and change the category of their fund allocation.

Nobody is truly willing to bet against these established tech giants.

The risk to their balanced sheet is obvious, but from the hyperscalers' perspective, it is better to improve CAPEX to overcome a scenario where the Labs build a moat through their own infrastructure, and render ‘the old’ cloud business obsolete.

The entry into data centers and power generation through nuclear power-purchase agreements (Microsoft with Constellation's Three Mile Island, Amazon with Talen's Susquehanna plant, Meta with Constellation), small modular reactor commitments (Amazon with X-energy, Google with Kairos Power, Meta with Oklo and TerraPower)[47], on-site gas and even fuel cells are all signs that for modern Cloud Business, the value-add is end to end, from energy to AI chips (Google TPU, AWS Trainium, Microsoft Maia, Meta MTIA) to servers to intelligence. It is a strategic move to own the entire supply chain and add more revenue streams.

Microsoft has learned its lesson through the collaboration with OpenAI, when the latter diversified to other partners, and even started DeployCo with consulting giants to expand its revenue stream beyond foundational models. Microsoft is doing the same by developing Maia 200 [46] to wean out of NVIDIA from 2026 to 2028.

With cloud costs rising, even before the integration of AI, news like Google's 78 percent cut in Gemini serving costs means little for the market, unless the cost cuts are passed on to the customers.

The biggest threats to the hyperscalers are open-weight models that could drive the cost of intelligence towards zero. The on-premise AI mandate and China’s constraints from not getting their hands on cutting-edge chips mean that the innovators in the next 2 years might disrupt the unit economics entirely, with AI turning into a low-margin utility service.

A cheaper intelligent service that could be run locally without high-cost infrastructure would end the bet on AI. And then we will see the crash, akin to the 2001 Dot Com burst.

Till then, Hyperscalers have a huge CAPEX and first movers advantage.

Implication for the Technologist

Technologists and applicants planning to enter the Technology industry must think like an architect. They are no longer a single product expert. They are the orchestrators, the scenario analysts, and a systems thinker who studies the market, the energy demand, technology integration, and funding/balance sheet impact from each solution. They are the modular version of CEOs with strong multi-functional thinking.

For Aspiring Technology Applicants

An applicant who is well-versed in engineering and capital structure, capable of arguing a choice, has a clear advantage where functional expertise in technology is no longer the only advantage.

Trend 2: The Agentic ROI Gap

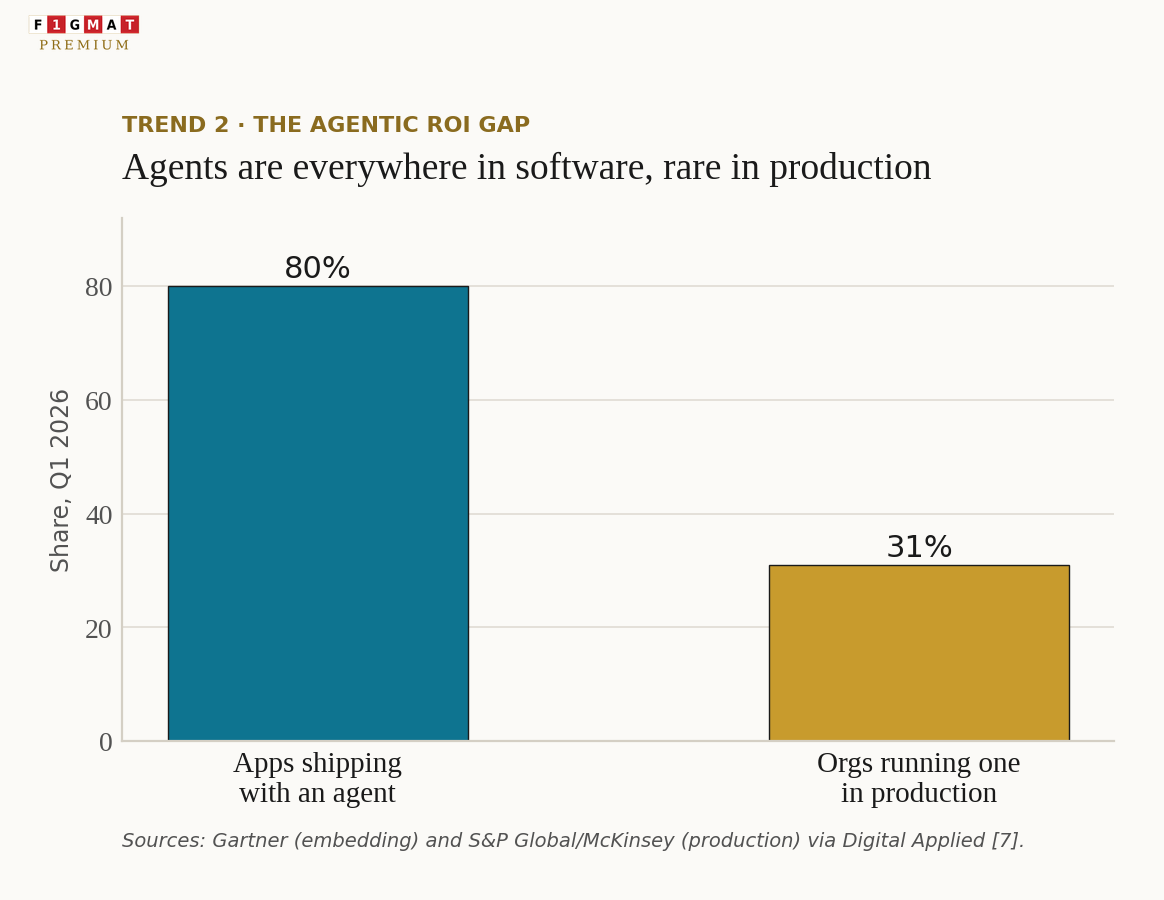

Agents became the default deployment package. Gartner reports that 80% of enterprise applications shipped or updated in Q1 2026 embed at least one AI agent, up from 33% in 2024 [7]. The trend is similar to the cruise control era, where every luxury or even mid-tier car had cruise control. Even in 2026, the adoption rate of this feature is low to really low.

In the enterprise market, Salesforce, SAP, and Microsoft have packaged Agents even if enterprise users are never going to use them.

The contrast is the adoption rate, where, according to S&P Global and McKinsey, the adoption rate is roughly 31% of organizations. Even within the organizations, banking and insurance leads (about 47%). Here risk of financial loss or lawsuits should have reduced the adoption rate, but the challenge for every vendor pushing for Agentic AI lies in the evolved processes the industries have adopted before AI arrived. In Banking and insurance, where automation software is in its fourth decade of iteration, processes have been optimized to the T, and repetitive workflows in reconciliation, fraud checks, and claims have already been perfected. Even the budgets for technology retainers are fixed, with in-house expertise available for deployment.

In Healthcare (18%) and government (14%) [7], the processes have not evolved. There is high-risk of leaking patient or citizen data. The liability clauses and serious harm to the public restrict Enterprise AI providers from keeping the Human in the Loop to a low number. In these two sectors, where procurement rules, privacy constraints, and upgradation of legacy systems require the influence of political leaders and senior bureaucrats, the friction to automation is high.

Why 95% of enterprise GenAI and 88% of agent pilots fail

MIT's 2026 study found that about 95% of enterprise GenAI pilots fail to deliver ROI, and a widely cited figure holds that 88% of agent pilots never reach production [7][8]. The largest contributing factor is the lack of trainable data. The data are siloed or lack the contextual knowledge AI desperately needs. Without the ‘context’ workflow, Agentic AI cannot work independently or with less than 40% human in the loop. Because these projects are in pilot, and the outcome determines the promotions or layoffs, employees don’t want to risk their promotion with untested frameworks or processes. There is no clear team ownership as the outcome does not just dependant on the employee’s orchestration or data labeling skills. 42% of firms abandoned most AI initiatives last year, up from 17%, and the average organization scrapped roughly 46% of proofs of concept before production [9].

What separates the winners

Where agents are scoped to real institutional data with defined tools, memory, permissions, and escalation paths, the returns are measurable.

The median time to realize a return is about 5.1 months, with sales-development agents paying back in 3.4 months and finance and operations agents in 8.9 months [7]. The initially instinct is to assume that enterprise sales are now automated. It is far from the truth. The initial grunt work of reaching out and warming up the lead is now done by the agent. The high ticket conversion still needs personality and persuasion to convert. The return in several such studies is the return on the investment made, not the positive ROI. Finance and Operations agents couldn’t scale, taking 8.9 months, as impersonal reaching out could erode trust when money or the stability of operations is concerned.

The contrarian study came from Anthropic's 2026 State of AI Agents report, which finds eight in ten organizations believe agents have already delivered measurable ROI, with the remaining barriers being integration (46%), data quality (42%), and change management (39%) [8].

It is easy to cite the three most important barriers to adoption while hinting that the organizations have achieved measurable ROI. But do remember the caveat. The study was conducted by surveying over 500 technical leaders across company sizes and industries in late 2025, with respondents including engineering leaders, IT executives, and technical decision-makers from startups to large enterprises across multiple sectors.

The difference between MIT’s study and Anthropic’s study is that the latter has already decided to incorporate Agents. Among the self-selected group, 80% realized their return.

The third survey that validates the for vs. against claims for AI agents is the Forrester report, which cites that enterprises plan to delay 25% of AI spend into 2027 as CFOs demand proof or ROI, noting only 15% of decision-makers reported an EBITDA lift in the prior year [9].

The Agentic AI replacing humans is far from reality in 2026.

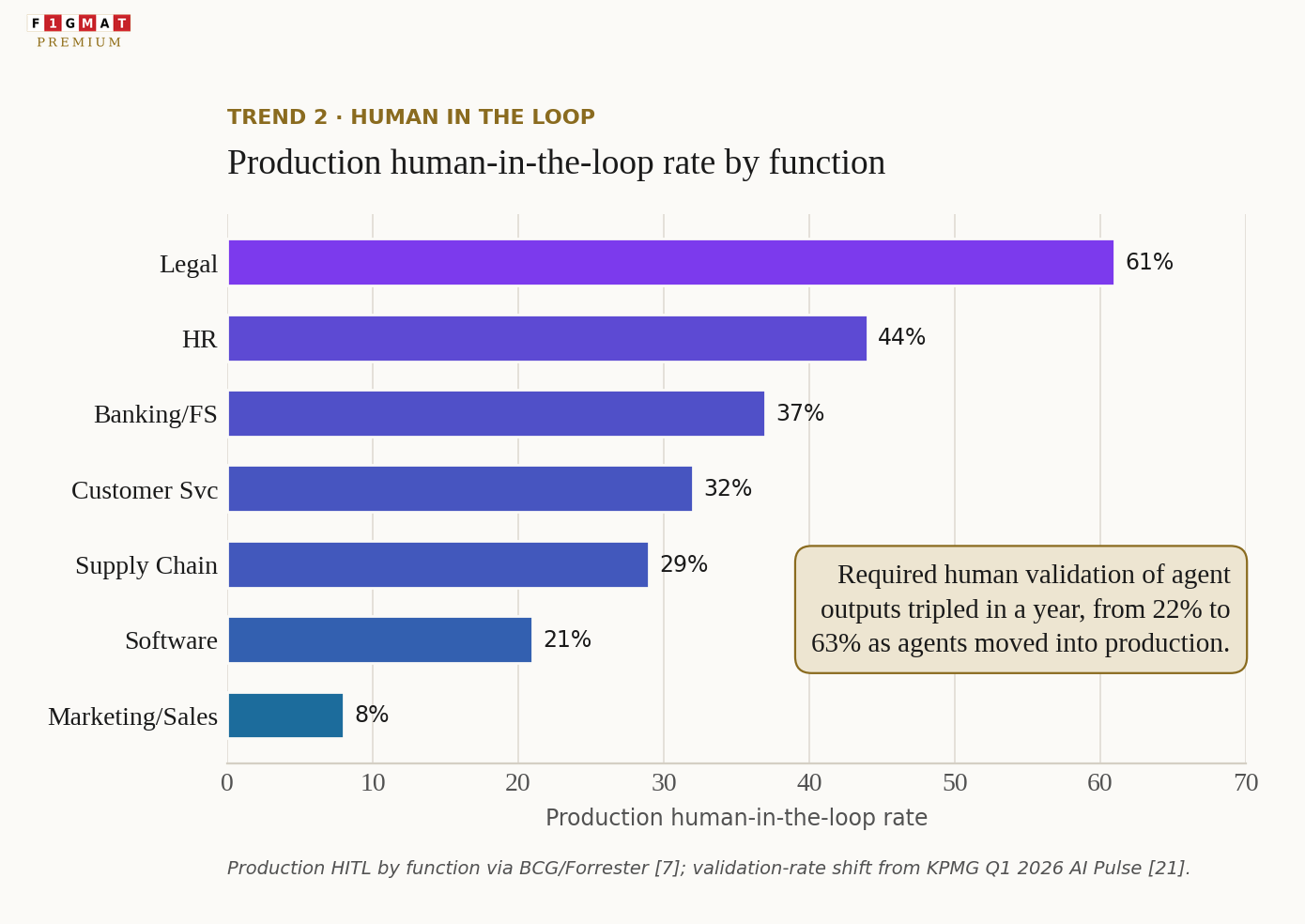

Human-in-the-Loop: Expectation versus Reality by Industry

A metric everyone concerned about mass unemployment from Agentic AI should monitor is the HITL or Human in the Loop percentage, as shown in the table below.

Organizations entered production assuming agents would run with light supervision. The pilot-era norm was roughly 22% of AI outputs were human-validated. Later in production, the demand was much higher.

KPMG's Q1 2026 pulse reports that 63% of organizations are not allowing AI agents access to sensitive data without human oversight, up from 22% a year earlier [21]. The transition from sandbox to production has introduced the cumulative error vector, where 95% reliability in one step could accelerate to 50% unreliability by step 10. The higher oversight from humans is both from regulation limiting autonomous agents from creating havoc without accountability, liability clauses limiting the risk-taking, and long-term reputational harm that the agents could cause the brand.

A January 2026 survey found that only 17% of workers consider workplace AI reliable without human oversight, and 64% expect the need for review to rise [22]. The feedback could have been contributed by the workers’ own fear that Agentic AI might replace their jobs. Even Anthropic's own telemetry shows the pattern is task-shaped, where about 87% of tool calls on simple tasks carry human involvement. This could be humans working on low-intensity cognitive tasks, not letting AI agents take over their responsibilities. It could also be that the simple tasks have high-cost consequences. The argument is that as users trust the output of the agents, they are granted greater autonomy, while complex tasks that have far higher consequences and complexity are offered full autonomy in 67% of cases [23].

The highest human oversight was in Legal and Compliance, where bias and unfair decisions could set new precedents that have systemic costs, while the lowest HITL was in Marketing and Sales, where the error in messaging could be an embarrassment, but the long-term costs are low in our attention-sparse society.

Software/Technology with predictable coding standards and debugging routines had the 2nd lowest Human in the Loop (HITL).

Customer Service and Support, which was earlier automated with chatbots, albeit the unintelligent ones, resurfaced with 32% HITL, clearly showing the value of Tier-1 human support in complex technology workflows. Again, the cost of an error had high consequences on the stability of systems.

Supply Chain Planning was the fifth niche under the 40% HITL, with Insurance Claims also mandating HITL to avoid bias and unfair decisions from producing discriminatory outcomes, as challenges to the Agentic AI-led decisions have high legal liability.

| Industry (dominant agentic use case) | Pilot expectation | Production reality (HITL) | Why the gap |

|---|---|---|---|

| Marketing and Sales (SDR, outbound, lead routing) | 5% HITL, fire and forget | 8% HITL [7]; most pilots still stall at 3 months without clean data | Narrow scope and reversible errors keep autonomy high, but data quality, not the model, decides success. |

| Software and Technology (coding, DevOps, test) | 10% HITL, near-autonomous | 21% HITL [7], code and security review | Production reliability and post-breach scrutiny pull review back in; agent runtimes now log every tool call. |

| Customer Service and Support (tier-1 deflection, triage) | 15% HITL | 32% HITL [7], escalation on edge cases | Brand and refund exposure force human handoff on complex or ambiguous tickets. |

| Supply Chain and Manufacturing (planning, N-tier mapping) | 20% HITL | 29% HITL [7] | Physical and tariff consequences require validation before a commitment is executed. |

| Banking and Financial Services (reconciliation, finance ops, fraud triage) | 20% HITL | 37% HITL [7] | Audit, model risk, and EU AI Act high-risk credit use cases require sign-off. |

| Insurance (claims intake, underwriting support) | 20% HITL | 40%+ HITL (est.) | Fairness obligations and Annex III classification raise oversight. |

| HR and People Operations (sourcing, screening, onboarding) | 25% HITL | 44% HITL [7] | Employment decisions are Annex III high-risk; bias and labor law force human review. |

| Healthcare and Life Sciences (prior auth, non-clinical ops, documentation) | 25% HITL | 50%+ HITL (est.) | Annex III high-risk rules, FDA software-as-a-medical-device limits, and HIPAA keep clinical actions human-led. |

| Legal and Compliance (contract review, regulatory research) | 30% HITL | 61% HITL [7], highest of any function | Liability and EU AI Act penalties (up to 7% of global turnover) demand step-by-step validation. |

| Government and Public Sector (eligibility, citizen service) | 20% HITL | Near-full oversight; 14% production adoption [7] | Accountability, procurement rules, and transparency mandates slow autonomy the most. |

HITL = human-in-the-loop. Sources: function-level production rates are BCG and Forrester telemetry compiled in Q1 2026 [7]; the aggregate shift in required human validation, from 22% to 63% year over year, is KPMG [21]; the finding that only 17% of workers consider workplace AI reliable without oversight, with 64% expecting review to rise, is Connext Global [22]; the task-complexity pattern (87% human involvement on simple tool calls versus 67% on complex) is Anthropic [23]. Rows marked (est.) for insurance and healthcare are inferred from high-risk (Annex III) oversight norms rather than a single published rate. Pilot-expectation values reflect the 22% pilot-era baseline [21], not per-industry figures.

Implication for the Technologist

The skill most in demand, ironically, is technical. You should learn to connect a model to CRMs, ERPs, ticketing tools, databases, and internal APIs by learning API design, authentication patterns, and the latest on Model Context Protocol (MCP), with at least mastery in one agent framework (LangGraph as a start). None of the technical skills matter if technologists don’t know how to write eval or cases to evaluate whether the input and the expected output match. The complementing skill is acquiring business sense. This is not an easy skill to acquire without understanding your company’s unique market position, strategy for growth in the next 2-3 years, and the automation opportunities. An MBA or a Consulting role will expand the exposure required to gain this business perspective.

For Aspiring Technology Applicants

It is tough to predict where Agentic AI will be in 2030. A reliable way to acquire skills in the latest framework and, throughout the journey, keep an eye on a new way of thinking where you can ingest frameworks, technology, and strategies in a much more efficient way than models can do is by mastering Systems thinking.

At its core, Systems thinking is the mental clarity to breakdown the messy world into its parts, design interventions, create feedback loops, and iterate to architect a solution that could be plugged into any industry or function. For Agentic AI, Systems thinking is in determining how to create systems that work with the lowest possible HITL percentage while also meeting all compliance and regulatory requirements.

An obsession to study the entire job function, moving parts in a job function, or critical interactions in an industry is required to acquire Systems thinking.

For Agentic AI, the judgment is in separating what humans can excel at and what models can excel at in a human-machine collaborative workflow. Designing solutions that are mindful of the ideal ways in which humans and agents collaborate is a foundational skill aspiring technologists must target. The skills are not entirely systems thinking. Technologists must also be interested in design, psychology, and be obsessed with efficiency every step of the way.

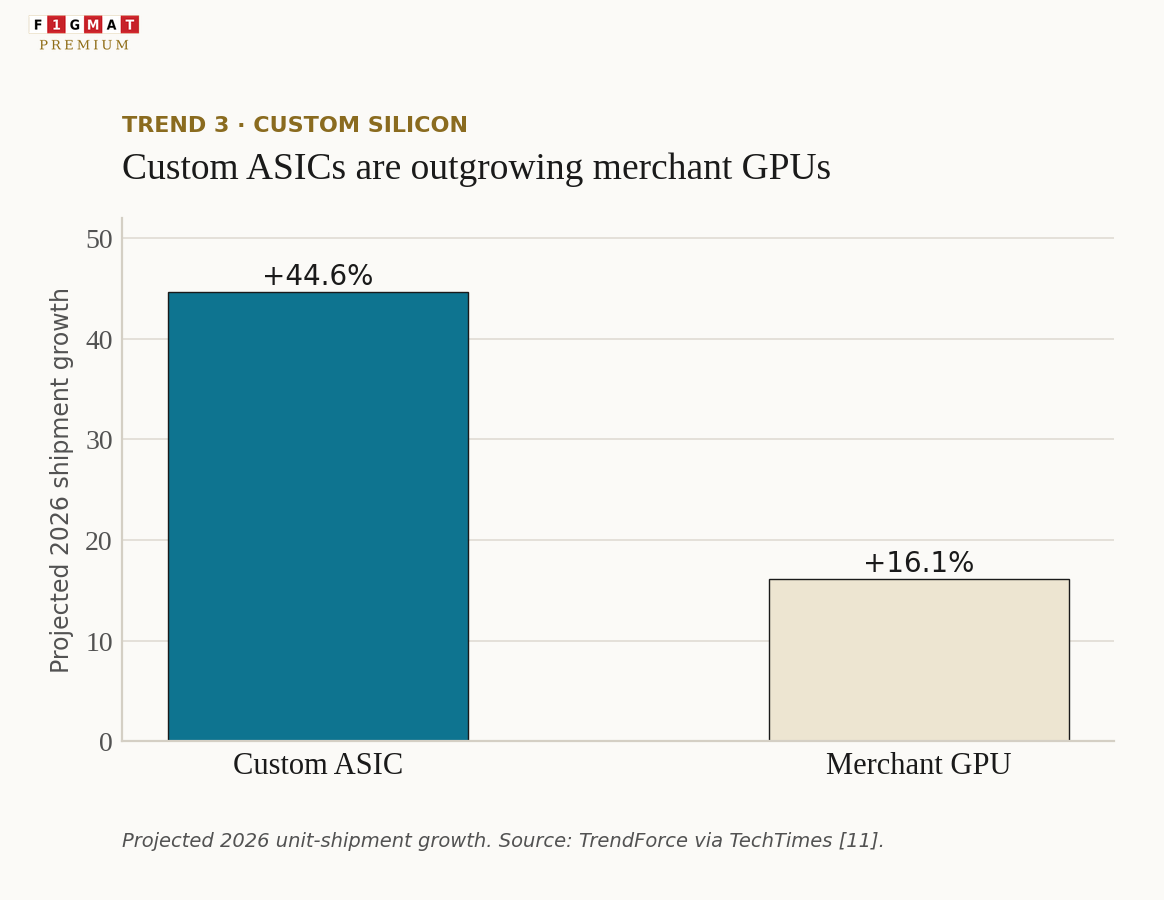

Trend 3: The Silicon Boom

The inflection point in 2026 is the divergence between custom accelerators and merchant GPUs. NVIDIA's advantage with close to 85% market share didn't bother Hyperscalers, as they themselves were testing with models that fit their organization or model release cycle. Once the giants perfected their models, an NVIDIA general-purpose GPU chip was a performance speed breaker.

On targeted inference benchmarks, custom accelerators have claimed several times the performance per watt of comparable Nvidia systems, with vendor figures of more than 4x against Hopper-class GPUs. A critical condition to optimize for performance is the match between the model and the chip's specialization. SambaNova, for instance, set an independently verified speed record on Llama 3.1 405B, running it several times faster than GPU-based providers on its custom chips [48]

Unlike NVIDIA's GPUs, which are engineered to handle any AI workload thrown at them, a custom ASIC is purpose-built for a specific model architecture, a specific inference pattern, or a specific training topology.

This is a reason why, for the first time, custom accelerators are outgrowing merchant GPUs offered by NVIDIA. TrendForce projects that custom ASIC shipments are set to rise 44.6% in 2026 against 16.1% for merchant GPUs, with ASIC-based AI servers reaching about 27.8% of the market, the highest share since 2023 [10][11].

Every major hyperscaler now designs its own silicon.

Broadcom and the co-design economy

Hyperscalers design the chips but rarely build them alone. Broadcom and Marvell together hold an estimated 95% of the custom ASIC co-design market [11]. Broadcom reported $8.4 billion in AI semiconductor revenue for Q1 fiscal 2026, up 106% year over year, guided to $10.7 billion for the next quarter, and cited a $73 billion backlog with a target to more than $100 billion in AI chip revenue in 2027 [10].

OpenAI signed a 10-gigawatt custom-accelerator collaboration with Broadcom, with first deployment targeting the second half of 2026, and Anthropic committed to roughly 3.5 gigawatts of TPU-based capacity beginning in 2027 [10].

NVIDIA's slow erosion

NVIDIA still holds roughly 70 to 86 percent of the AI accelerator market, depending on the segment measured, and its general-purpose GPUs run any workload while a custom ASIC is tuned for one customer [10].

Analysts expect its share to slip toward the 70 to 80 percent range by 2028 as custom silicon takes two to three years to develop and Nvidia refreshes its architecture every 12 to 18 months [11]. This is a share of a market that is itself expanding.

NVIDIA's unit volumes keep rising even as the percentage drifts down.

Do custom ASICs de-risk the TSMC bottleneck?

Custom accelerators are co-designed by Broadcom and Marvell, but almost all of them (Google TPU, AWS Trainium, Microsoft Maia, Meta MTIA, and OpenAI's Broadcom-built chip) are fabricated by TSMC, which produces roughly 90% of advanced AI logic at 7nm and below [25].

Moving from Nvidia GPUs to in-house ASICs changes who designs the chip, not who manufactures it. The shift concentrates demand on the same foundry in Taiwan.

The chokepoint is two layers deep.

Beyond leading-edge logic, advanced packaging is the problem that Hyperscalers are expecting from GPU makers.

NVIDIA alone is expected to support about 60% of 2026 CoWoS packaging capacity, with Broadcom and AMD taking another quarter, which leaves little for smaller ASIC vendors even as TSMC scales toward 100,000-plus CoWoS wafers per month [24]. The scarcity drives TSMC's pricing power, with advanced-node wafer prices rising 5 to 10 percent in 2026 and a 2nm wafer passing $30,000 [25].

This makes Taiwan the single most important strategic partnership for the US.

Samsung Foundry is ramping a 2nm process and bundling high-bandwidth memory with capacity to win non-flagship and some AI work, while Intel Foundry markets its 18A node and EMIB packaging as a second source, though its yields trail TSMC, and few expect it to be credible for mission-critical silicon before 2027 to 2028 [25].

The practical option is that customers route lower-end and less-critical chips to Samsung and Intel while keeping flagship AI parts on TSMC.

Geographic de-risking through TSMC's $165 billion Arizona cluster adds US logic capacity, but most advanced packaging continued to stay in Taiwan.

The supply chain's center of gravity has barely moved [24].

China's Bet on Advanced packaging and System architecture

China's answer to being locked out of cutting-edge chipmaking is to change the game rather than win it on the West's terms.

Blocked from EUV lithography, the chipmaking technology produced solely by the Netherlands' ASML, and unable to fabricate the smallest transistors, Chinese researchers and companies are betting on advanced packaging and system architecture instead. In one approach, a domestically-designed 14nm logic chip is stacked onto 18nm DRAM using 3D hybrid bonding[49], which its designers claim rivals Nvidia's 4nm silicon at roughly 120 TFLOPS. Huawei pushed the same logic further in May 2026 with an engineering technique it calls "LogicFolding," aimed first at its Kirin smartphone chips[50]. Both sidestep the lithography barrier by assembling older nodes more cleverly over iterating towards smaller transistors.

NVIDIA Introduces NIM microservices

NVIDIA understood the competition from ASIC and moved into models and software. Its Nemotron 3 models come in three sizes (Nano, Super, and Ultra) and are open-weight. Companies can download and run them freely.

The unique positioning is in how NVIDIA's mid-size model with 120 billion parameters can be used as a service. Unusually for a chipmaker, NVIDIA also publishes the training data and methods behind the models [26].

The advantage for NVIDIA is distribution. The company packages its own and third-party models (Llama, DeepSeek, Qwen, Mistral) as NIM microservices, GPU-optimized containers with an OpenAI-compatible API that deploy on any Kubernetes cluster with Nvidia GPUs, and on-premises or air-gapped models for regulated industries that cannot send data to a public cloud [26].

The effect is a deeper moat.

Nemotron's real-time inference runs on Nvidia GPUs.

Every open model Nvidia releases makes its hardware stickier to an enterprise AI scaling effort. As custom ASICs chip away at GPU share, Nvidia is widening the surface it sells (models, the NeMo tooling, NIM serving, and robotics stacks), which lets it lose accelerator market but still capture more of each AI dollar in regulated industries.

Implication for the Technologist

With hyperscalers using ASICs to build their own chips, away from Nvidia GPUs, like Google TPUs, AWS Trainium, Microsoft Maia, and Meta MTIA, the technologist's job is to map each workflow to the right combination of hardware and model, or open or closed models, which could improve productivity and accuracy of delivering a task.

For Aspiring Technology Applicants

Understanding why a company would spend billions designing its own chip should be the starting point for learning about technology stack strategy and long-term brand objectives.

The solution should be built around the company's strategic objective.

Candidates should reason across silicon, supply chain, and model distribution, and not just be limited by one 'new' technology stack or a programming language.

Trend 4: The Power-and-Cost Squeeze, Grid Backlash Meets FinOps 2.0

AI's costs moved out of private credit and onto the public.

Wholesale power on PJM, the largest US grid serving 67 million people across 13 states, averaged $136.53 per megawatt-hour in Q1 2026, up 76% from $77.78 a year earlier, according to the grid's independent monitor [12].

The US residential rate reached 17.45 cents per kWh in January 2026, a 9.5% year-over-year increase that outpaced inflation [13].

Grid Inefficiency

Data centers now consume about 6% of US electricity, and Lawrence Berkeley National Laboratory projects the figure could reach 6.7 to 12 percent by 2028 [14].

The interconnection queue, the median wait to connect new generation to the grid, has stretched to roughly 54 months in 2026 from 22 months in 2000, even as a data center can be built in about two years [14].

North Carolina State University researchers estimate data-center demand could raise power costs by 6 to 29 percent nationally and up to 57 percent in some regions by 2030, and the Dallas Fed warns wholesale prices could rise as much as 50 percent as demand doubles [14]. The result is a political backlash, with utilities proposing their first base-rate increases in decades.

Delay in AI Spending

Inside the enterprise, the same pressure shows up as cloud-cost.

Forrester expects firms to delay a quarter of planned AI spend into 2027 and reports that fewer than one in three can tie AI value to profit-and-loss changes [9].

CIOs cite technical complexity (26%), security and privacy (26%), and uncertain ROI (24%) as the top barriers to scaling AI. For each outcome – good, bad and worst, these leaders had to shift to scenario-based budgeting and cost-per-AI-feature accounting [9].

The caution came from Technical complexity (26%) where the time it takes to integrate models, clean data and rebuild workflow is hard to predict. Even worse, Security and privacy (26%) in AI systems, earlier contained with safe model integration practices was disrupted with the arrival of Agentic AI. The moment agents touch real data and take actions autonomously in a way that is different from the caution and real-world consequence a human worries about, new attack patterns from prompt-injection to violating data privacy (GDPR, the EU AI Act, sector rules) emerged. But the most obvious reason to push back AI spending to 2027 is from uncertain ROI (24%).

After the 2025 wave of failed pilots, CIOs learned that AI spending often didn't produce measurable return. The uncertainty has now crystalized to one metric – the payback period. By making the Payback period the be all metric, companies can compare their pilot period with the production timeline.

The alternatives energy sources tech firms are pursuing and lobbying for

With grids saturated and interconnection queues measured in years, the industry is funding an unusually wide set of workarounds.

Goldman Sachs shared that the reversal is a boon for nuclear, geothermal, fuel cells, and storage as hyperscalers and governments are now forced to diversify procurement [30]. In the near term, the default fallback is on-site fossil generation.

Meta is funding roughly ten gas-fired plants for a single Louisiana campus and Google is building gas capacity beside a North Texas site, which keeps emissions rising even as cleaner options are promised [33].

The cleaner near-term substitute is the fuel cell.

Bloom Energy units deploy in as little as 50 days and let a data center run as an island off the grid, turning siting from a grid-access problem into a business decision [30].

Beyond the diversification in energy sources, the more striking move is offshore data center development.

Aikido Technologies plans to house 10 to 12 megawatts of compute inside the buoyancy tanks of floating offshore wind platforms, with a 100-kilowatt prototype slated for the North Sea off Norway, while Panthalassa raised $140 million (backed by Peter Thiel and Marc Benioff) for wave-powered floating nodes. Shipping firms are repurposing old cargo vessels as floating data centers [31][33].

Offshore appeals because seawater cooling is free, impact to coastal residents stays low, and the compute sits out of sight of the communities now resisting build outs of data centers near their communities.

Space-based data centers remain conceptual, held back by launch cost and latency.

The push to source or supply their own power ahead of the midterms, is from the realization that if Trump is voted out because of the public grid backlash, the entire momentum - a free regulatory reign on human automation will hit a wall. Energy is just a smaller battle against the War to make AI the new internet[33].

| Approach | What it is | Status in 2026 | Lead players |

|---|---|---|---|

| On-site gas | Behind-the-meter gas turbines beside the campus | Deploying now; emissions rising | Meta (Louisiana), Google (Texas) [33] |

| Fuel cells | Grid-independent on-site power, 50-day install | Commercial, scaling | Bloom Energy and AI-sector buyers [30] |

| Small modular reactors | Firm, carbon-free nuclear (covered in Q4 2025) | Commercial deployment 2030 to 2035 | Meta, Microsoft, Amazon nuclear deals [30] |

| Enhanced geothermal | Drilling to tap the Earth's heat anywhere | Pilots running | Google with Fervo (Nevada), Meta [30][33] |

| Offshore and floating | Compute on wind platforms, wave buoys, or ships; seawater cooling | Prototypes 2026 to 2028 | Aikido, Panthalassa, Mitsui OSK, Keppel [31][33] |

| Space-based | Orbital data centers on solar | Conceptual; latency and launch cost | Early-stage proposals [31] |

| Demand flexibility | Curtailing compute load during grid stress | In use | Google and utility partners [30] |

Implication for the Technologists and Consultants

Power and cost are now concerns for technologists. Token maxing has an upper bound. Companies were forced to cancel model subscriptions when usage was designed as the only KPI. Companies are looking for technologists who can prioritize solution architecture and models in such a way that cost and latency are optimized for higher ROI.

The technologist owns the FinOps layer from routing inference to finding the cheapest model for the task. Killing idle GPU clusters or allocating the right task for the cluster is now as important as reporting cost per feature spend over older methods of aggregate cloud spend.

For Aspiring Technology Applicants

Learn the unit economics of AI.

On the grid side, you should be able to discuss $/kW, interconnection queues, and why Northern Virginia and parts of Texas have paused new projects.

On the cloud side, you should know the reasons for higher token costs, capacity waste, and scenario budgeting.

The applicant who treats energy and FinOps as part of the core technology skills will fit into a new-world economy where companies are constantly trying to balance human with compute cost.

Trend 5: The Open-Weight Cost Collapse and Sovereign-AI Geopolitics

The price of frontier intelligence fell off a cliff.

DeepSeek V4 shipped as an open-weight, trillion-parameter model with a one-million-token context window at roughly $0.14 per million input tokens, about one-twentieth the price of leading closed models, and benchmarks near the prior frontier generation on math and question-answering [15].

Qwen 3.5 followed with a 397-billion-parameter mixture-of-experts model under an Apache 2.0 license, a 256K context window, and support for more than 200 languages [15].

Where Chinese and American models are winning

The competition in AI between China and America is ironically between American closed labs (OpenAI, Anthropic, and Google) and Chinese open-source families (Qwen, DeepSeek, and Kimi).

Western enterprise deployments still dominate the AI market, where reliability, support, and procurement relationships influence the deal more than the cost per token.

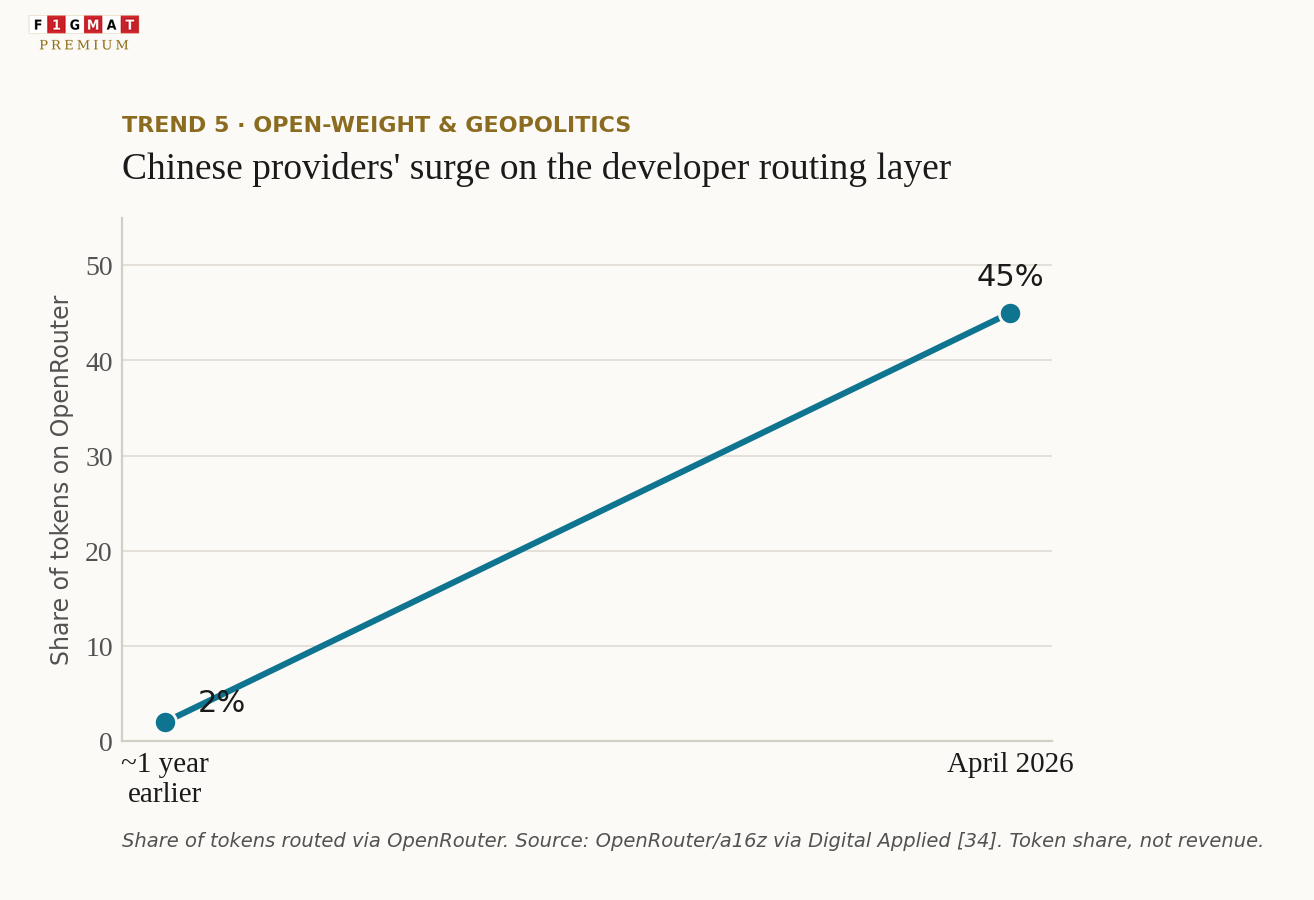

Chinese open-weight families are winning the developer and cost-sensitive SMB market. According to OpenRouter, the platform where developers let an automated router pick preferences among competing models, Chinese providers climbed from under 2% of tokens a year earlier to more than 45% by April 2026[34]. The shift was confirmed by a RAND study, which found the Chinese model's share jumped from 3% to 13% in the two months after DeepSeek's release. And it was uneven by geography, and preferred in regions where Western platforms reach less easily, with Chinese providers holding more than 20% of users across eleven countries by late 2025 [35].

Cost was not the only factor.

Alibaba's Qwen spawned more than 180,000 derivative models and overtook Llama in download velocity, while Meta pulled back from open releases (withholding its largest model and moving its next generation to a closed API), which ceded open-weight leadership toward China and prompted Nvidia's Nemotron as a US open response [34][37].

Usage and benchmark leadership have decoupled.

The highest-volume open models are typically not featured in the top 10 ranking for intelligence, as buyers benchmark against cost and then on specific strengths like coding and context window for the particular task [34].

| Region or layer | Who leads | What is driving it |

|---|---|---|

| North America | US closed labs (OpenAI, Anthropic, Google) | Enterprise reliability and procurement ties; Chinese models a cost-optimized minority via routing platforms. |

| Europe | US labs in enterprise; rising sovereignty push | Data-residency rules favor on-premises and open models; Mistral and EU efforts plus Chinese open weights for fine-tuning. |

| China | Domestic models (Qwen, DeepSeek, Xiaomi, Zhipu, Kimi, Hunyuan) | US models largely excluded; state-aligned funding and open releases as ecosystem tools. |

| Middle East | Multi-sourced; sovereign-funded build-out | Capital backing both US and Chinese stacks while building domestic infrastructure. |

| Global South (SE Asia, South Asia, Africa) | Chinese open models gaining fastest | Cost decides; over 20% user share in 11 countries; subsidized adoption in some markets. |

| Developer / API layer (global) | Chinese open-weight models | 45%+ of OpenRouter tokens; usage optimized for blended cost, not benchmark rank [34]. |

Regional read compiled from OpenRouter and Andreessen Horowitz usage data via Digital Applied [34], RAND and OpenRouter figures via NewMR [35], Microsoft adoption data via Visual Capitalist [36], and the US-China Economic and Security Review Commission analysis of open-model strategy [37]. Shares reflect usage on routing platforms and surveyed adoption, not revenue.

The two-tier market is developing so that high-volume work is routed to low-cost open models (often Chinese) and to closed, high-stakes US models for the hardest tasks, with on-premises or air-gapped deployment where data residency rules apply.

Compute and Open Source become Leverage

DeepSeek's ability to train competitive models without top-tier NVIDIA hardware is an attempt to undercut the premise that US export controls are determining AI global leadership. Globally, countries are investing in their own data centers and models to reduce dependence on both the US and Chinese stacks.

The two superpowers are now pursuing opposite strategies.

China subsidizes model adoption. Shenzhen offered up to 40% reimbursement, capped at $275,000 a year for companies building on a leading open-source agent stack as a hook to expand the Chinese AI ecosystem [34].

The US, on the other hand, works through restriction and private capital, tightening chip export controls and leaning on its frontier labs and hyperscalers to win the market through superior benchmarks.

Implications for the Technologist and Consultants

The technologist should now be capable of designing a routing layer that matches each task to the cheapest model, keeping inference options open if the tasks fail or don’t meet the quality standards. They should also know when to adopt closed providers, as on-premise or air-gapped deployments are mandatory for projects with data residency requirements.

For Aspiring Technology and Consulting Applicants

Inference economics is the new learning goal.

You should be able to run the arithmetic on a real workload, explain when self-hosting beats an API, and articulate the open-versus-closed tradeoff on cost, control, and capability.

You should also understand geopolitics to decode export policy, sovereign cloud preferences, and what that means when infrastructure gets built for the enterprise or a client.

Trend 6: The Entry-Level Erosion and the Reshaping of Post-MBA Finance and Consulting Roles

The labor effect of AI is first felt by entry-level professionals.

Employers disclosed about 54,836 AI-attributed layoffs in 2025, but modeling-based estimates place actual AI-displaced or foregone positions at 200,000 to 300,000, roughly 0.13 to 0.20 percent of US nonfarm employment, with the gap showing why firms rarely attribute automation as the cause [18][19] to avoid legal liability.

The 2026 pace did not slow down, with about 45,000 tech-sector layoffs by March [18].

Cutting in anticipation

A January 2026 Harvard Business Review survey of 1,006 executives found that only 2% reported large headcount reductions tied to actual AI implementation; far more reported slower hiring or cuts because they expect AI to change staffing later [19]. Again, the survey response could be a dressing-down effect to avoid legal liability. With highly trainable technology talent, the change in staffing layer is an excuse for overhiring during the pandemic and in anticipation of higher compute costs that a high-labor company cannot sustain.

Goldman Sachs estimates that AI is already reducing United States employment by roughly 16,000 jobs each month, a steady erosion that the bank attributes to automation of tasks. In another survey, about 37 percent of business leaders say they anticipate replacing at least some of their workers with AI by the end of 2026. The shift will be on a larger scale as agent deployments move from pilots into full production [19][18].

Why were Finance and Consulting Roles affected?

AI disproportionately exposes educated, white-collar tasks and the entry tier of finance and consulting functions.

Junior finance roles in analysis, compliance, and document review are among the most exposed.

PwC data shows roughly fourfold productivity growth in AI-augmented financial roles, which means firms need fewer people in entry roles, which have already been taken over by AI [18].

Wall Street banks have signaled plans to remove approximately 200,000 roles over three to five years, concentrated in entry-level and back-office functions [19].

In consulting, the junior research, deck-building, and first-draft analysis that defined the analyst year is now obsolete, pushing the value of a post-MBA hire toward judgment and client relationships. Anthropic's CEO has forecast that AI could eliminate half of entry-level white-collar jobs within five years [19].

The upside: positioning for the new entry-level

The picture is not all bleak.

Talent leaders are roughly 2.7 times more likely to say AI will increase entry-level hiring than decrease it, and 27% of firms that expect to expand junior hiring name greater AI use as the single biggest driver [39].

Workers with advanced AI skills earn about 56% more than peers in the same role, and productivity has nearly quadrupled in the industries most exposed to AI [40]. The work that survives and pays is the work AI cannot yet do well, which is judgment, interpretation, and knowing when an output is wrong.

A survey of 500 managers who hire MBAs put the 2026 priorities in order

- AI fluency (35%)

- the ability to quantify business impact (31%)

- A portfolio of applied work (25%)

Nearly a quarter now treat AI proficiency as a baseline expectation rather than a differentiator factor for an interview [38].

The most-cited gaps in recent hires were people leadership and coaching, and hands-on AI tool proficiency, which is precisely where a well-chosen MBA or Master's can close the skill gap [38].

Implication for the Technologist, Finance Associates, and Consultants

| Fading (what AI now does) | Rising (what entry-level should build) |

|---|---|

| Producing first-draft analysis, models, and decks | Directing and auditing agent output, with the judgment to catch what is wrong |

| Manual data gathering and research | Framing the problem and validating AI-gathered evidence against sources |

| Executing a single tool or task | Orchestrating multi-agent workflows across tools and systems |

| Generic, transferable domain familiarity | Deep, sector-specific expertise that becomes the durable moat |

| Being measured on volume of output | Being measured on quantified business impact and ROI |

| Solo technical depth | AI fluency paired with communication, coaching, and governance literacy |

For an applicant, the lesson is to stop competing for the entry-level work that AI is eliminating and instead arrive ready for the tier above it, which makes the choice of an MBA or a Master’s program a strategic decision.

The degree itself no longer sets a candidate apart, since AI fluency has become a baseline expectation. A curriculum where AI runs through the core over a single elective, and, more importantly, experiential projects that leave behind a visible portfolio of experiences where AI was integrated in real projects, is important for the candidate to grow beyond “knowing AI”.

The proof is in a body of work that shows you scoped a workflow, directed the agents, and measured what it returned.

The same logic points to the skills most candidates neglect.

Employers report that the widest gap in recent graduates is in people leadership and coaching skills, which is precisely the capability that gains value as the routine work is automated, and managing the change through coaching becomes the new responsibility.

Combine the leadership with a governance credential, such as the IAPP AI Governance Professional or ISO 42001 internal auditor, and the candidate with a top brand MBA or Master’s program will have deep sector judgment, the ability to direct agents, and the discipline to quantify impact for consulting, technology, and techno-financial roles. [38][40].

For Aspiring Technology Applicants

For applicants pivoting from finance or consulting into technology, expect the post-MBA responsibilities, at least in the short-term, to shift towards AI product management, agent design, and AI-augmented strategy.

The applicant should demonstrate judgment and AI fluency early in their career. Later, when AI becomes just another software tool that improves your productivity by let us say 30%, they should have the instinct to scope where automation helps, where it harms, and how to redeploy people who could be in a unique position to take over tasks where AI has failed.

Trend 7: The Compliance Cliff, EU AI Act Meets Agentic Deployment

The EU AI Act follows a phased timeline where prohibited practices took effect on February 2, 2025, and general-purpose model obligations plus governance infrastructure on August 2, 2026

The high-risk obligations, covering Annex III systems in employment, credit, biometric identification, and critical infrastructure [16], with provider requirements under Articles 9 to 17, deployer requirements under Article 26, and human-oversight design under Article 14, were scheduled to become enforceable on August 2, 2026 [16].

EU AI Act - A moving deadline

On May 7, 2026, EU lawmakers reached a political agreement to delay key deadlines[16][17]. This is because the technical standards that companies need to comply with (being written by the EU standards bodies CEN and CENELEC) were themselves delayed as 2025 saw a sustained push by US tech lobbyists with the message that European industry would be behind if the Act becomes too interventionist.

It was not just the influence of American technology companies; these rules had extraterritorial reach similar to GDPR, where any organization whose AI output affects EU residents falls in scope, regardless of where its servers run.

The standards must be carefully calibirated to avoid overreach as in the European Commission 2026 Competitiveness Report [51], the Commission itself admitted that Europe "risks losing its edge in the race for innovation," citing labour shortages, scale-up problems, low patent applications, and R&D spending below the 3%-of-GDP target, and noted Europe is strong in AI research papers while the US dominates in AI companies and China in rapid deployment and scale.

Europe is officially worried that the regulation would permanently keep Europe dependant on China and the US, just like they were dependant on Russia and the Middle East for Oil and Gas.

Why Agentic deployment raises regulatory stakes

Autonomous agents make the compliance requirements even more complicated, as an agent that acts in a high-risk domain (screening candidates, scoring credit, managing critical infrastructure) can easily take steps that could trigger conformity assessment, documentation under Article 11, human oversight under Article 14, and post-market monitoring. Each regulatory step slows down the effectiveness of an AI agent, which was introduced to the workflow to replace humans' limitations in memory, energy, and motivation.

Cybersecurity is the 2nd largest barrier. ISO 42001 emerged as the practical management-system standard that satisfies Article 17 and integrates with existing ISO 27001 and 9001 programs.

Implication for the Technologist and the Consultant

Governance is now an architecture requirement.

Explainability of an agentic behavior, human-in-the-loop checkpoints, comprehensive logging, and post-market monitoring have to be designed into agentic systems from the first sprint, as retrofitting these guardrails into a black-box model in a high-risk context is far harder.

The technologist who can map an agent's actions to Article 14 oversight obligations and stand up an ISO 42001 management system turns compliance into a deployment advantage for the company.

For Aspiring Technology Applicants

For product-management and architecture roles, fluency in the human-oversight and logging requirements, and in ISO 42001, is a clear skill advantage as governance becomes a recurring operating cost.

Key Takeaways

1. Constraint replaced capability as the story.The limits that defined Q1 2026 were physical and financial: power on the grid, capital structure on the balance sheet, and governance in the deployment pipeline. Model quality was rarely the bottleneck.

2. Scale was rewarded, half-measures were not.Capex concentrated in the Big Five, agent ROI concentrated in production deployments rather than pilots, and inference economics split between commodity open-weight workloads and premium frontier tasks.

3. The professional bar moved.The technologist who advances in 2026 is fluent across the stack: silicon and routing, capital and FinOps, energy and governance. Narrow technical depth without that context is a weaker hand than it was a year ago.

What to Watch into Q2 2026

- Capex versus monetization: Whether AI revenue growth begins to close the gap with the $660 to $690 billion 2026 capex commitment, and whether circular-financing scrutiny forces cleaner revenue disclosure [2][5].

- Agent production rate: Whether the share of organizations running agents in production climbs from 31% as tooling matures, or whether the pilot-to-production gap persists [7][8].

- Silicon multi-sourcing: How fast custom ASIC share rises against Nvidia's general-purpose lead, and whether interconnect standards let custom chips clear at scale [10][11].

- Grid backlash.Whether PJM, Texas, and other regions impose data-center cost allocation or siting limits as consumer power bills keep rising [12][14].

- The EU AI Act timeline.Whether the May 2026 political agreement to delay is formally adopted, and how the high-risk obligations land for agentic systems [16][17].

References

- Goldman Sachs, Why AI Companies May Invest More than $500 Billion in 2026

- CreditSights, Technology: Hyperscaler Capex 2026 Estimates ($602B, 75% AI) ↩ ↩ ↩ ↩ ↩ ↩

- Futurum, AI Capex 2026: The $690B Infrastructure Sprint ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Introl, Hyperscaler CapEx Hits $600B in 2026 (debt issuance, January 2026 update) ↩ ↩ ↩

- Bloomberg, AI Circular Deals: How Microsoft, OpenAI and Nvidia Keep Paying Each Other ↩ ↩ ↩ ↩ ↩ ↩

- INSEAD Knowledge, Are We in an AI Bubble? ↩

- Digital Applied, AI Agent Adoption 2026 (Gartner, S&P Global, BCG, Forrester data points) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Anthropic, The 2026 State of AI Agents Report ↩ ↩ ↩ ↩

- Forrester, Predictions 2026: AI Moves From Hype To Hard Hat Work ↩ ↩ ↩ ↩

- Tom's Hardware, The Custom AI ASIC State of Play (Broadcom, Google TPU, Meta MTIA) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- TechTimes, Custom AI Chips Outpace Nvidia GPU Growth in 2026 (TrendForce) ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Bloomberg, Data Centers Push Power Bills Up 76% on Largest US Grid (Monitoring Analytics) ↩ ↩ ↩ ↩ ↩

- Electrek, Data Centers Are Cutting Power to Homes (residential rate data) ↩ ↩ ↩

- Belfer Center, Harvard, AI, Data Centers, and the U.S. Electric Grid: A Watershed Moment ↩ ↩ ↩ ↩ ↩

- Particula, DeepSeek V4 and Qwen 3.5: Open-Source AI Is Rewriting the Rules in 2026 ↩ ↩ ↩ ↩ ↩

- Cloud Security Alliance, EU AI Act High-Risk Compliance Deadline ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Travers Smith, EU Agrees to Delay Key AI Act Compliance Deadlines (May 7, 2026) ↩ ↩ ↩ ↩

- Yale Insights, The Real Job Destruction from AI Is Hitting Before Careers Can Start ↩ ↩ ↩ ↩ ↩ ↩

- finflowmax, How AI Is Eliminating White-Collar Jobs (2025-2026 Data) ↩ ↩ ↩ ↩ ↩ ↩

- NC State University, Data Centers Are Driving Up Power Bills: A New Study

- KPMG, Q1 2026 AI Quarterly Pulse Survey (human validation of agent outputs rose from 22% to 63%) ↩ ↩ ↩

- Connext Global, 2026 AI Oversight Survey (only 17% consider workplace AI reliable without oversight) ↩ ↩

- Anthropic, Measuring AI Agent Autonomy in Practice (human involvement by task complexity) ↩ ↩

- 24/7 Wall St., AI Chip Packaging Constraints and TSMC CoWoS Concentration (Nvidia 60% of 2026 CoWoS demand) ↩ ↩

- DigiTimes Asia, TSMC Faces AI Supply Strain as Samsung, Intel, and Apple Test Foundry Alternatives ↩ ↩ ↩

- NVIDIA Newsroom, NVIDIA Debuts Nemotron 3 Family of Open Models (NIM microservices, deploy anywhere) ↩ ↩

- SaaStr, Anthropic Passes OpenAI in Revenue (WSJ financials: OpenAI $14B 2026 loss, $1T+ infrastructure commitment) ↩ ↩ ↩

- Sacra, OpenAI Revenue, Valuation and Funding (OpenAI $25B ARR Feb 2026; Anthropic run-rate) ↩ ↩ ↩

- Software Thug, AI Company Financials: Spending, Losses, Profitability (burn rates; xAI loss ratio) ↩

- Goldman Sachs, Accelerating Power Demand From Data Centers Boosts New Energy Technologies ↩ ↩ ↩ ↩ ↩ ↩

- Singularity Hub, Investors Bet $140 Million on Data Centers at Sea (Panthalassa wave-powered floating compute) ↩ ↩ ↩

- OilPrice, Big Tech Is Funding Space Solar and Fusion While Running on Gas (Meta gas plants, geothermal, energy pledge)

- Digital Applied, Chinese AI Models Q2 2026 Market Share Report (OpenRouter 45%+, Xiaomi 21%) ↩ ↩ ↩ ↩ ↩ ↩

- NewMR, Chinese AI Models Are Reshaping the Global Landscape (RAND and OpenRouter usage data) ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Visual Capitalist, Mapped: AI Adoption by Country in 2026 (Microsoft data) ↩ ↩

- US-China Economic and Security Review Commission, Two Loops: How China's Open AI Strategy Reinforces Its Industrial Dominance ↩

- CSP Global, More Employers Plan to Hire MBAs in 2026 and AI Fluency Is Now the Baseline ↩ ↩

- Strada Education Foundation, Entry-Level Hiring in the AI Era (AI more likely to increase than reduce entry-level hiring) ↩ ↩ ↩

- Kelly / Gloat, Skills Employers Want in 2026 (durable judgment skills; 56% AI skills pay premium) ↩

- Meta Platforms, Q1 2026 Results (revenue $56.31B, 2026 capex guidance $125B to $145B, FCF and cash) ↩ ↩

- Microsoft, FY2026 Results 8-K (AI run-rate $37B, up 123% YoY; Azure growth) ↩ ↩ ↩

- Synergy Research / Gotrade, AWS vs Google Cloud vs Azure: Hyperscaler Stocks 2026 (cloud share, RPO) ↩ ↩

- Amazon Q1 2026 earnings analysis (AWS $37.6B, operating income $14.2B, AI run-rate $15B, backlog $364B) ↩

- Oracle, FY2026 Q1 Results (RPO $455B up 359%, OCI projected $18B, capex) ↩ ↩

- The AI Capex Boom: Bubble or Infrastructure Supercycle?" ↩ ↩

- The Rise of Custom AI Chips Is Breaking Nvidia’s Grip ↩ ↩

- Every Nuclear-Powered Data Center Deal: Google, Amazon, Meta & Microsoft (2026) ↩

- SambaNova breaks Llama 3 speed record with 1,000 tokens per second ↩

- Tom's Hardware, "China claims domestically-designed 14nm logic chips can rival 4nm Nvidia silicon" (Nov 28, 2025) ↩

- CNBC, "Huawei plans new smartphone chips this fall as rivalry with Nvidia and Apple heats up" (May 25, 2026) ↩

- Why is the EU struggling to scale artificial intelligence? ↩