As we close the first quarter of 2026 for the Investment Banking industry, global M&A reached an estimated $1.6 trillion in announced deal value, a 50.6% year-on-year increase and a new quarterly record.

TL;DR

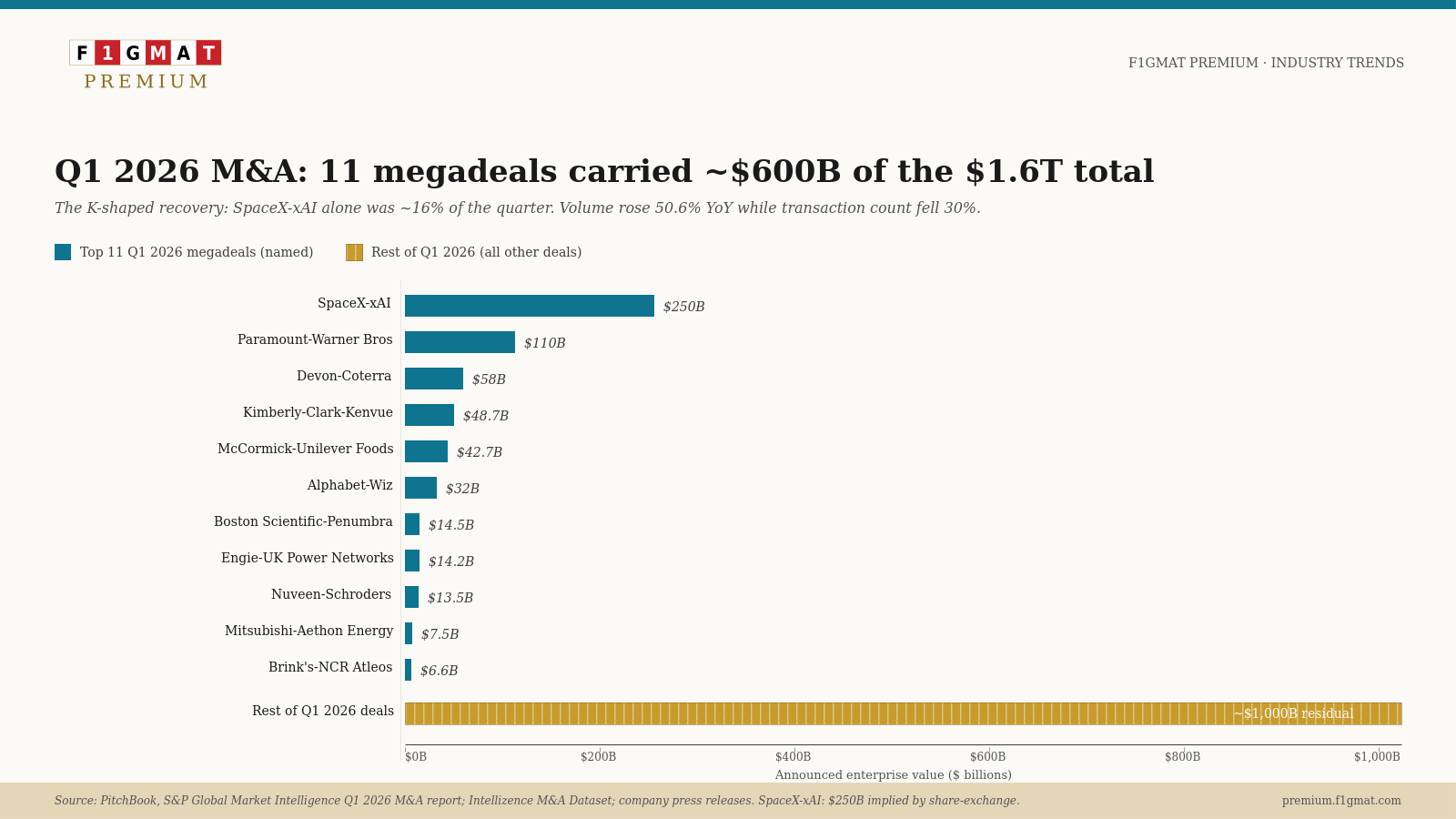

• Megadeal concentration. Global Q1 M&A hit $1.6 trillion announced (+50.6% YoY, a record), but transaction count fell 30% YoY. SpaceX-xAI alone accounts for ~30% of total Q1 deal value

• IB earnings surge. The strongest Q1 IB hiring environment in four years. Goldman advisory +89%, Morgan Stanley advisory +74%, JPMorgan markets a firm record at $11.6B, Citi best Q1 in a decade.

• AI infrastructure capex doubles. $660-725 billion across the Big Five hyperscalers in 2026, nearly double 2025. Power is now the binding constraint. Microsoft holds $80B in unfulfilled Azure orders due to a lack of grid capacity

• ECM reawakens selectively. US ECM had its best Q1 in five years ($9.4B from 22 IPOs), where $31B was in convertible issuance alone. The comeback was led by power infrastructure, defense, and convertibles.

• Bespoke capital architecture: Megadeals now require layered structures where private credit is a regular feature. Even more surprising was when JPMorgan disclosed $50B private credit exposure within $160B of non-bank lending

• GENIUS Act operational. Stablecoin supply hit $315B. The OCC granted national trust bank charters to Circle, Paxos, BitGo, Ripple, and Fidelity. Tokenized deposits emerge as the bank counter-product

• Basel III re-proposed. On March 19, 2026, the Fed/OCC/FDIC re-proposed the US bank capital framework, reducing aggregate capital requirements at the largest US banks by ~6%. Comments due June 18, 2026.

We observed 7 trends shaping the quarter:

Trend 1: The K-Shaped M&A Market and the Megadeal Concentration

Trend 2: Investment Banking Earnings Surge as the M&A Drought Ends

Trend 3: AI Infrastructure Capex Doubles to $660-725 Billion

Trend 4: ECM Reawakens with Selectivity, Defense and Convertibles Lead

Trend 5: Bespoke Capital Solutions and Private Credit Convergence

Trend 6: GENIUS Act Implementation Phase Begins as Stablecoins Hit $315B

Trend 7: Basel III Revision, US Banking Capital Re-proposed

Trend 1: The K-Shaped M&A Market and the Megadeal Concentration

Q1 2026, with the total announced deal value at $1.6 trillion, a 50.6% jump year-on-year[6], was the strongest opening quarter for global M&A by value since 2021. Even on a traditional and stricter metric of completed transactions, Q1 2026 reported $861.1 billion in deals, up 9.7% YoY[7]

Despite the record value in deals, the transaction count fell 30% YoY to 7,924, the lowest activity count in years[7].

The SpaceX-xAI Transaction

The single transaction that defined the quarter was SpaceX's all-stock acquisition of xAI, announced in February 2026. The deal valued SpaceX at $1 trillion and xAI at $250 billion, creating a combined $1.25 trillion entity[11]. S&P Global reports that the xAI portion alone accounted for nearly 30% of total Q1 deal value[7]. The deal is functionally an internal Musk-empire consolidation, but its sheer scale distorts every market-level metric for the quarter.

Paramount Acquires Warner Bros. Discovery

On February 27, 2026, Paramount Skydance and Warner Bros. Discovery (WBD) signed a definitive merger agreement under which Paramount will pay $31.00 per share in cash for WBD, valuing the target at $81 billion in equity value and $110 billion in enterprise value, representing a 7.5x multiple on fully synergized 2026 EBITDA[10]. The transaction is the largest media merger ever signed. Paramount funded a $2.8 billion termination fee to release WBD from a prior agreement with Netflix, an unusual structural feature that signals how aggressive megadeal sponsors are willing to be in 2026[10].

Megadeal Volume Outpaces Total Deal Volume

The K-shape economy of the main street was visible in Wall Street too, where mega deals drove $1B+ deals in just January and February 2026, 57% ahead of the same period in 2025. Even the transaction count was higher - 22 vs 14 in 2025 [15]. From the 23 financial-services megadeals in Q1 2026[6], the energy sector led Q1 2026 M&A growth with value up 59.8% quarter-over-quarter

Implication for the Investment Banker

Because the deal count has gone down, bankers negotiating mid-market deals are at a greater risk of redundancy than bankers in JPMorgan or boutique banks specializing in large deals in niche sectors.

The bulk of advisory fees went to boutique and large banks.

For post-MBA opportunities, the implication is that sector specialization in consolidating verticals (AI infrastructure, biopharma, energy) carries more career leverage.

For the Aspiring IB Applicant

For applicants targeting IB out of an MBA program, the K-shaped market changes are an opportunity to facilitate deals in consumer durables and home appliances that typically face consolidation, while the luxury and premium travel segment gains revenue. The high-income households driving the K-Shaped market drives higher likelihood of mega deals in cross-sector consolidation in the luxury and premium market segments.

Identify the groups that won the SpaceX-xAI, Paramount-WBD, and Abbott-Exact Sciences advisory roles.

For the SpaceX xAI Merger, Morgan Stanley worked with both sides of the deal. Elon Musk has a long history of working with the bank [17].

Prioritize MS Technology desks where the priorities are in space-tech and AI infrastructure.

For the Paramount (Skydance) Warner Bros. Discovery (WBD) merger, the players were diverse. On the buyer side, for the Paramount/Skydance side, it was Centerview Partners, who led and were supported by RedBird Advisors, with BofA, Citi, M. Klein & Co., and LionTree. The seller side of the deal for WBD was led by J.P. Morgan, and supported by Allen & Company and Evercore [18]

Candidates from Media and Entertainment pivoting to an IB advisory role must prioritize Centerview. JP Morgan played a supporting role.

For healthcare candidates, the Abbott Exact Science merger was driven by Morgan Stanley, which was also the exclusive financial advisor and financier. On the sell side, Centerview Partners was the lead, while supported by XMS Capital Partners [19]

BoFA[23] led the McCormick-Unilever deal, widening the options available for candidates planning to get hands-on experience in CPG, which is likely to see more such consolidation in an down economy.

Study the background on the mergers, the drama around the Netflix vs. Paramount (Skydance) stand to control WBD. The interviewer prefers to understand candidates' interest in the structure of a mega deal over technical formulas like the DCF.

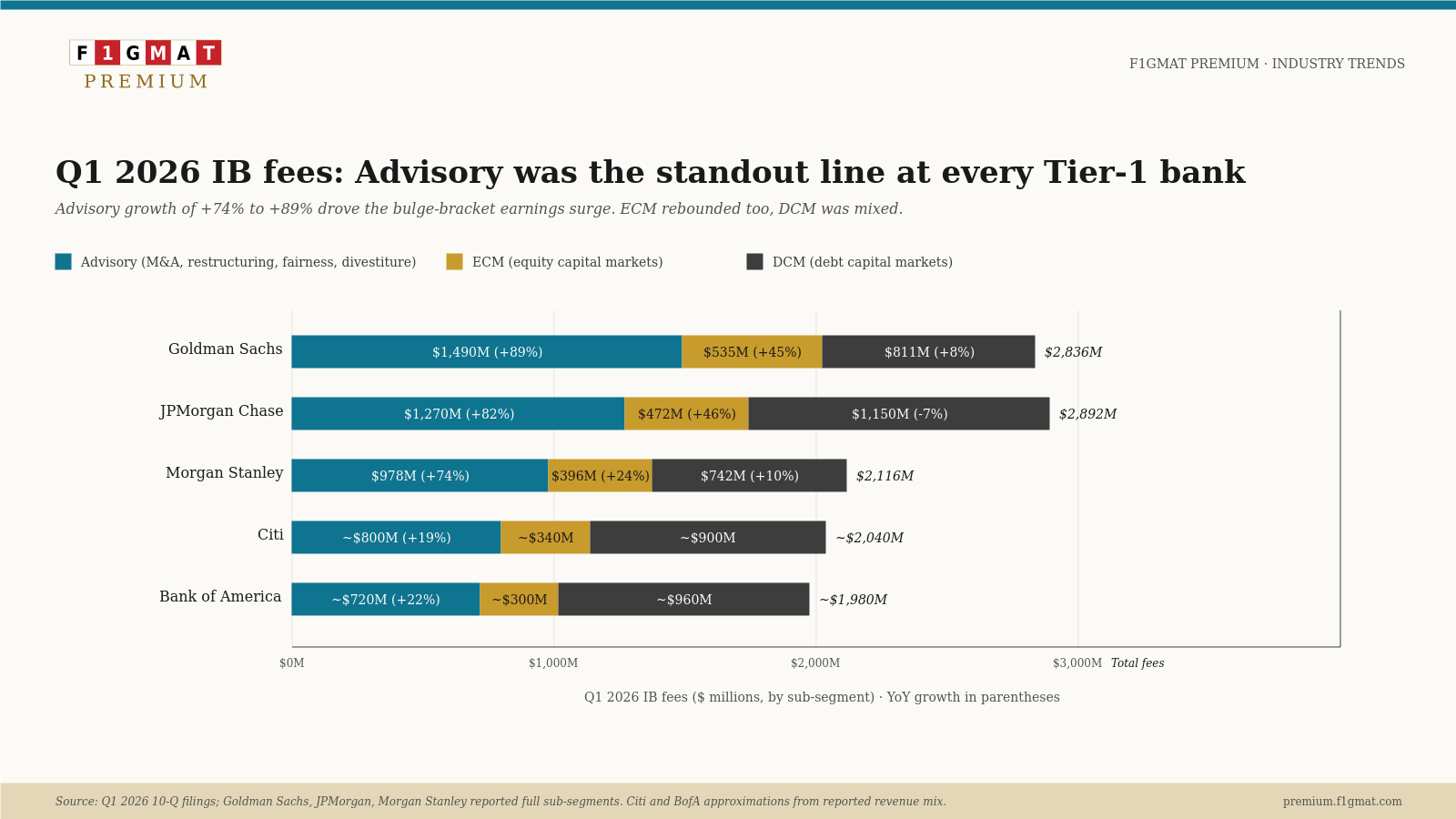

Trend 2: Investment Banking Earnings Surge as the M&A Drought Ends

Q1 2026 confirmed that the multi-year advisory drought is decisively over.

Every Tier-1 bank reported double-digit IB revenue growth, with advisory the standout revenue item.

What is covered under banking advisory fees

• Goldman "Financial advisory" explicitly mentions M&A plus other strategic advisory (restructuring, spin-offs, defense)

• JPMorgan"Advisory" cites M&A and other corporate advisory services

• Morgan Stanley "Advisory" services include M&A, divestitures, restructuring, and corporate defense

• Citi"Advisory" services include mergers and acquisitions, divestitures, restructurings and corporate defense activities

Q1 2026 Revenue Comparison Across Major US Investment Banks

In bulge bracket banks, 80-90% of advisory services are M&A related. The remaining services are related to restructuring, divestiture, defense (against hostile takeover from activist investors), and fairness-opinion work (a report on whether the terms of the deals are fair to all shareholders)

Investment Banking Fees Breakdown

Even if there are several services within an Investment banking deliverable, broadly, the IB Fees are classified into Advisory (M&A), ECM (equity underwriting), and DCM (debt underwriting).

All YoY versus Q1 2025.

Table A: Underwriting revenue

| Bank | Total Revenue | Total IB Fees | Advisory (M&A + restructuring + defense) | ECM (Equity Underwriting) | DCM (Debt Underwriting) |

|---|---|---|---|---|---|

| Goldman Sachs [2] | $17.2B (+14%) | $2.84B (+48%) | $1.49B (+89%) | $535M (+45%) | $811M (+8%, IG and asset-backed) |

| JPMorgan Chase [1] | $49.8B (+10%) | $2.88B (+28%) | $1.27B (+82%) | $472M (+46%) | $1.15B (-7%, lower leveraged finance) |

| Morgan Stanley [3] | $20.6B (record) | $2.12B (+36%) | $978M (+74%) | $396M (+24%, IPOs + convertibles) | $742M (+10%, IG event-driven) |

| Citigroup [4] | $24.6B (+14%) | +12% YoY | +19% (best Q1 in a decade) | +64% (follow-ons, convertibles) | -6% (lower non-investment-grade) |

| Wells Fargo [5] | $21.4B (+6%) | CIB banking revenue +11% | Not disclosed separately | ECM market share rose vs FY25 | Not disclosed separately |

| Bank of America [23] | $30.3B (+7%) | $1.8B (+21%, excl. self-led) | Combined within Advisory line | Reported in Global Banking | Reported in Global Banking |

CIB: Corporate and Investment Banking

As expected, in Bulge Bracket Banks, Advisory (M&A plus restructuring and corporate defense) was the strongest IB Fee factor with Goldman reporting +89%, JPMorgan +82%, Morgan Stanley +74%, and Citi +19% in revenue growth YoY. Citi’s revenue growth in Q1 is the largest in a decade.

ECM or Equity Underwriting was the second-strongest source of revenue, driven by convertibles and follow-ons.

Traditional IPOs, which used to be a large part of the ECM revenue have crashed.

In the AI-driven economy, only PE-funded firms could drive IPOs. Even in such a constrained environment, Goldman +45%, JPMorgan +46%, Citi ECM +64% all reported above 40% growth.

DCM performance was underwhelming. The leveraged-loan market without the support of PE firms has remained muted. Only Goldman +8% and Morgan Stanley +10% benefited from investment-grade and asset-backed issuance.

JPMorgan -7% and Citi -6% lagged on weaker non-investment-grade issuance.

Investment Banking Trading Revenue by Fixed Income and Equities

The sales and trading revenue is a different sub-item compared to IB fees. For the breakdown, we have to look at the fixed income (FI) and Currencies & Commodities (FICC) vs. Equities revenue.

Table B - Trading revenue (Markets)

Trading revenue (Markets) in total including FI, FICC, and Equities, is different from underwriting revenue (Table A).

| Bank | Total Markets Revenue | Fixed Income (FICC) | Equities |

|---|---|---|---|

| Goldman Sachs [2] | $9.3B combined | $4.0B (-10%) on weaker rates and mortgages, offset by currencies and commodities gains | $5.33B (+27%, record quarter); equities financing record at $2.61B |

| JPMorgan Chase [1] | $11.6B (+20%, firm record) | $7.1B (+21%) on commodities, credit, currencies and emerging markets | $4.5B (+17%) on increased client activity |

| Morgan Stanley [3] | $8.5B (+27%) | $3.36B (+29%, post-crisis record) on commodities volatility | $5.15B (+25%, record) on prime brokerage and derivatives strength |

| Citigroup [4] | $7.2B (+19%) | $5.2B (+13%) firm-wide; ranked #2 globally in FI | $2.1B (+39%) firm-wide; ranked #6 globally in Equities |

| Wells Fargo [5] | +19% YoY (CIB Markets segment) | Not disclosed separately at firm level | Not disclosed separately at firm level |

| Bank of America [23] | $6.4B (+13%, best quarter in 15 years) | $3.5B (+2%) on credit and currencies activity | $2.83B (+30%, record) on volatile-market client flows |

Goldman, which led on Advisory and ECM, posted the weakest FICC result at -10% on lower rates and mortgages revenue.

Every other bank showed double-digit FICC growth.

Equities were strong across the board, with both Goldman ($5.33B) and Morgan Stanley ($5.15B) setting franchise records on volatility-driven prime brokerage and derivatives flows.

JPMorgan's $11.6B in combined Markets revenue was a firm record.

The pattern shows that 2026 rewards different trading desks than 2025: commodities and currencies inside FICC, prime brokerage and derivatives inside Equities.

Goldman Sachs

Goldman reported total IB fees of $2.84 billion, up 48% YoY, with Global Banking & Markets net revenues at $12.74 billion, up 19% YoY[2].

Three factors drove the result:

• Accelerated M&A closures. The smoother regulatory approval process contributed the most to the IB fee strength [1]. The lower debt underwriting volume also forced the organization to hike the fee, which also contributed to the growth of IB fees.

• Convertible-led equity underwriting. Equity underwriting was $535 million, up 45% YoY, primarily reflecting convertible offerings[2]. Issuers took advantage of strong equity market conditions and investor appetite for hybrid securities amid volatility.

Convertibles provided a risk-averse option for companies seeking lower coupon rates with the potential to increase the upside of equity movements.

• Record equities trading. Equities revenue reached $5.33 billion, up 27% YoY, with strength across both intermediation and financing on volatility-driven client flows. This was a record quarter for the franchise[2].

JPMorgan Chase

JPMorgan posted Q1 2026 IB revenue of $3.1 billion, up 38% YoY, with IB fees of $2.88 billion, up 28% YoY[1]. The result was the highest IB fee figure of any global bank in the quarter per Dealogic. Three factors drove it:

• Accelerated M&A closures. Management attributed IB fee strength to faster-than-anticipated regulatory approvals that pulled forward closing dates from later in 2026[1]. Advisory and equity underwriting fees both rose, partially offset by lower debt underwriting.

• Record markets revenue. Markets revenue was $11.6 billion, up 20% YoY (a firm record). Fixed Income led at $7.1 billion, up 21%, on strong commodities, credit, currencies and emerging markets activity. Equities reached $4.5 billion, up 17%[1].

• Improving credit quality. The provision for credit losses fell 24% YoY to $2.5 billion, with $139 million of consumer reserve releases. The lower credit cost dropped through to a 13% rise in net income to $16.5 billion, freeing capital for client lending and buybacks[1].

Morgan Stanley

Morgan Stanley reported a record quarter at $20.6 billion in revenue, $3.43 EPS and 27.1% ROTCE[3]. Institutional Securities delivered record revenues of $10.7 billion. Three factors drove the result:

• Advisory broadening across sectors. Advisory revenues reached $978 million, up 74% YoY, with CFO Sharon Yeshaya noting that completed M&A activity broadened across sectors with notable strength in technology and industrials[3]. Investment Banking revenues totaled $2.12 billion, up 36% YoY.

• Record equities trading. Equity revenues climbed 25% YoY to a record $5.15 billion on strength across cash, derivatives, and prime brokerage. Fixed income produced post-crisis record revenues of $3.4 billion[3].

• Wealth Management asset gathering. Wealth Management revenue reached a record $8.52 billion, up 16% YoY. Net new assets were $118.4 billion in the quarter, with $54 billion of fee-based asset flows. Total client assets across Wealth and Investment Management approach $10 trillion[3].

Citigroup

Citigroup posted its strongest first-quarter revenue in a decade at $24.6 billion, up 14% YoY, with net income of $5.8 billion, up 42%[4]. Three factors drove the result:

• Banking strength led by advisory. Banking revenue rose 15% YoY. IB fees rose 12%, M&A advisory fees rose 19% (Citi described it as the strongest first quarter for advisory in a decade), and ECM rose more than 60% on stronger sponsor activity[4].

• Markets revenue surge. When markets swing a lot, clients trade more actively. Citi captured a large share of this extra trading volume as Equities revenue jumped 39% to $2.1 billion (beating estimates by ~$500 million). With the volatility in oil prices, clients were hedging and repositioning their bond and commodity positions, which again benefited Citi, whose Fixed Income rose 13% to $5.2 billion. In total, Markets' revenue rose 19% YoY [4].

• Services and Wealth contribution. Services revenue rose 17% to $6.1 billion, exceeding expectations on treasury and trade solutions activity. Wealth revenue rose 11% (the eighth straight quarter of growth), with $15 billion in net new investment asset flows[4].

Wells Fargo

Wells Fargo reported diluted EPS of $1.60, up 15% YoY, and net income of $5.3 billion. Total revenue grew 6% to $21.4 billion.

Within Corporate and Investment Banking, segment revenue rose 4% with banking revenue up 11% YoY[5]. Three factors stand out:

• ECM share gains. Wells Fargo disclosed that its overall Investment Banking market share held stable at 4.3% while ECM market share rose versus FY25, indicating continued share capture in a category historically dominated by JPMorgan, Goldman, and Morgan Stanley[5].

• Fixed Income and Equities Revenue Grew: Markets revenue rose 19% YoY on stronger client activity, lifted by both fixed income and equities. The pickup followed the December 2025 Fed rate cut and March 2026 oil-price volatility[5]. A lower rate triggers bond price hikes. With yields falling for products with short-term and intermediate maturities, corporations, hedge funds, and investors reposition their portfolios as a hedge against duration risk. The Oil price volatility that weakens U.S Dollar and supports commodity price increases drives hedging and trading activities. Both these activities drove the revenue of Wells Fargo’s FICC bucket, which rose 15% YoY to $1.583 billion, with clear strength in commodities, credit, and rates.

• Back to New Business After Last Consent Order. Wells Fargo had many consent orders because of the big fake accounts scandal in 2016 (employees opened millions of accounts without customer permission)[20]. In Q1 2026 (specifically March 5, 2026), the Federal Reserve officially ended the last remaining consent order from 2018[21]. This was the 14th consent order Wells Fargo has successfully closed since 2019. It means the bank has now completed almost all the major regulatory punishments and fixes required after the scandal. For years, these consent orders and an asset cap (a limit on how big the bank could grow) held Wells Fargo back. The bank couldn’t easily open new branches, hire lots of people, or grow its business aggressively because regulators were watching closely. Closing the final consent order removes the last big restriction.

Wells Fargo is now free to grow normally like its competitors (JPMorgan, Bank of America, etc.). As a result, the firm added approximately 200 commercial bankers over the prior 18-24 months and reported early signs of higher new-client acquisition[5].

Bank of America

Bank of America posted Q1 2026 net income of $8.6 billion (+17% YoY), revenue of $30.3 billion (+7%), and diluted EPS of $1.11 (+25%). Total Corporation IB fees of $1.8 billion rose 21% YoY, beating the consensus of $1.73 billion, and Markets revenue of $6.4 billion was the strongest quarterly trading result in 15 years[23]. Three factors stand out:

• Lead advisor on the McCormick-Unilever Foods deal: BofA was lead financial advisor and primary liquidity provider on McCormick's $42.7 billion acquisition of Unilever's food business (announced April 2026), and also advised on Boston Scientific's $14.5 billion Penumbra acquisition and Devon Energy's $26 billion combination with Coterra. The bank provided a $15.7 billion bridge facility on the McCormick deal, which positions it for top-3 league-table placement in CPG M&A for 2026[23].

• Record equities trading: Equities revenue rose 30% YoY to $2.83 billion, beating estimates by roughly $350 million. Total sales-and-trading revenue of $6.4 billion (+13%) was BofA's strongest quarter in 15 years, driven by client activity during March 2026 oil-price volatility. FICC revenue was $3.5 billion (+2%) on credit and currencies strength[17].

• Methodology note on the 21% headline number: BofA's 8-K aggregates debt advisory, equity advisory, and M&A advisory into a single Advisory line, rather than the M&A-led Advisory plus separate ECM/DCM convention used by Goldman, JPMorgan, Morgan Stanley, and Citi. The +21% growth headline reflects the aggregate IB fee pool of $1.8 billion (excluding self-led deals), not pure M&A advisory. For peer comparisons, BofA's IB fee total sits closest to Citi's +12% total IB fee growth and below Goldman's $2.84 billion total IB fees (+48%)[23].

Implication for the Investment Banker

The revenue rebound is concentrated in Advisory (M&A) and ECM.

Goldman noted that debt underwriting was higher overall but with significantly lower revenue from leveraged finance, indicating that the leveraged loan market has not yet caught up with strategic M&A.

For Bankers placed in advisory groups (M&A, restructuring, capital structure) at Tier-1 firms, Q2 2026 is the first quarter where they can fulfill their role with fewer uncertainties. Deal flows are stronger, the compensation structure is revised, and there is a clearer career path, ending the uncertainty they faced since 2021.

For the Aspiring IB Applicant

The 2026 hiring cycle is the strongest IB hiring environment in four years.

Tier-1 firms have expanded analyst classes, lateral hiring at the associate and VP levels has accelerated, and Wells Fargo's hiring of approximately 200 commercial bankers over the prior 18-24 months shows broader expansion at the next tier.

As IPOs are unlikely to come back in large volumes, most of the IB activities will be concentrated in advisory (M&A) and ECM roles. The commodities volatility and policy uncertainty have guaranteed that DCM activity will not come back any time soon, especially if the war in Iran persists. Leveraged Finance is now strictly the purview of PE professionals.

But since the deal flow is at a multi-year high, execution readiness through technical skills, domain exposure, deal process exposure, and modeling speed carries more real-world value.

Choose MBA and Master's Curriculums based on these four skills.

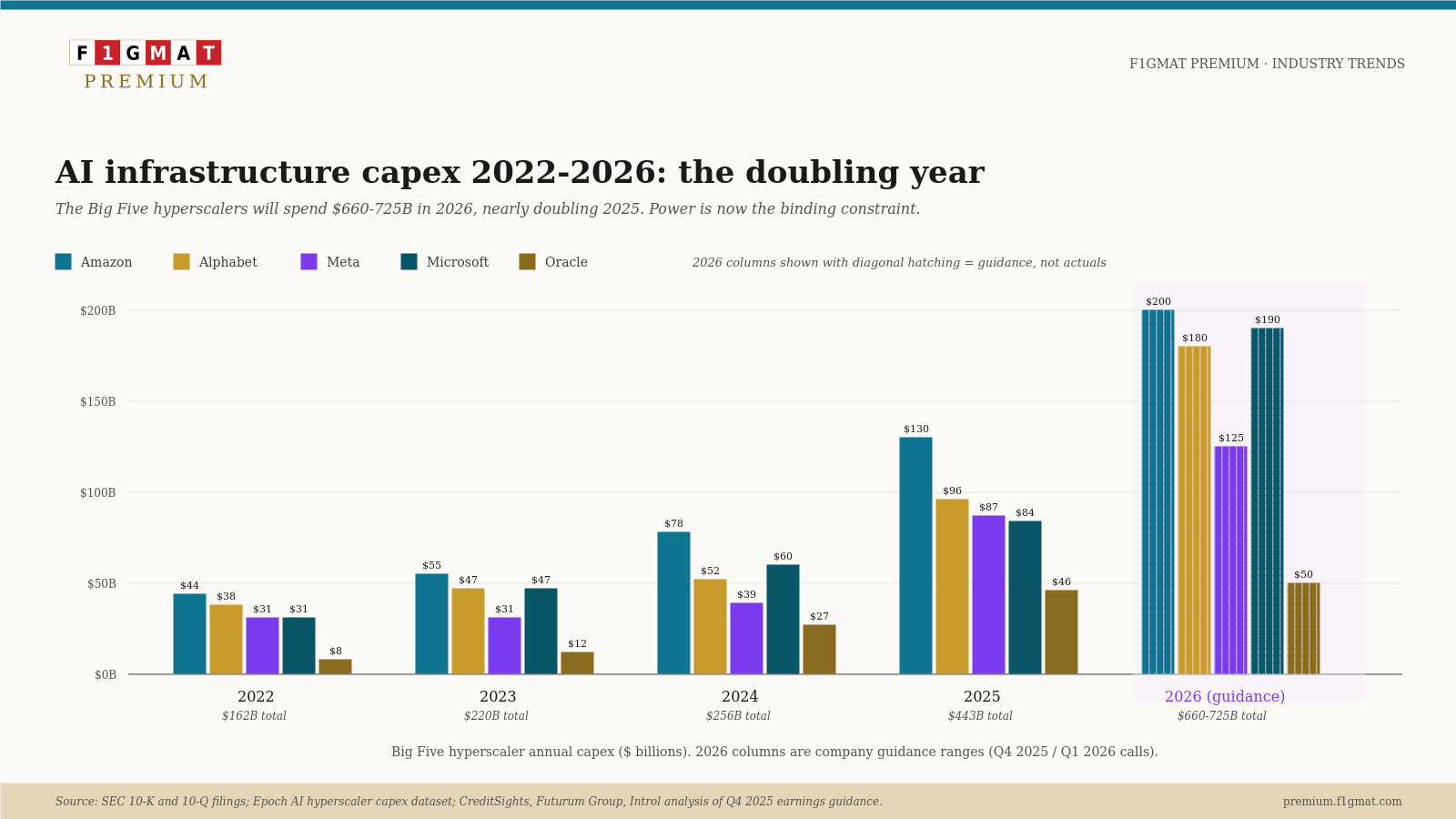

Trend 3: AI Infrastructure Capex Doubles to $660-725 Billion

The AI infrastructure super-cycle introduced in Q4 2025 went into overdrive in Q1 2026. Combined 2026 capex plans for the Big Five hyperscalers (Microsoft, Alphabet, Amazon, Meta, Oracle) now sit at $660 to $725 billion, nearly double the $443 billion they collectively spent in 2025[14].

Table C - Hyperscaler Capex Per Firm (2026 Guidance)

| Firm | 2026 Capex Guidance | Q1 2026 Notable Detail |

|---|---|---|

| Amazon (AWS) | ~$200 billion | AWS revenue grew 28% YoY in Q1 2026. |

| Alphabet (Google Cloud) | $180-190 billion | Google Cloud revenue grew 63% YoY in Q1 2026 to $20 billion. Lifted 2026 capex by $5 billion in mid-quarter guidance. |

| Meta | $115-135 billion | Stock fell 6% on capex jump and roadmap concerns. |

| Microsoft | ~$120 billion+ | Microsoft spent $11.1 billion leasing data center space in Q1 2026 alone. Holds $80 billion in unfulfilled Azure orders due to power constraints. |

| Oracle | ~$50 billion | Announced workforce reduction of 20-30K tied to AI data center funding shortfall. |

Power Infrastructure Becomes the Binding Constraint

The most important shift in Q1 2026 was the transition from a chip-supply bottleneck to a power-supply bottleneck.

Microsoft's $80 billion in unfulfilled Azure orders is contracted demand that the firm cannot serve until new data centers come online with sufficient electrical capacity[14].

Northern Virginia and parts of Texas have stopped accepting new data-center projects entirely because they have exhausted available grid capacity[14].

Bankers are now structuring grid-connection deals, power-purchase agreements with nuclear operators, and sale-leasebacks of data-center real estate.

Implication for the Investment Banker

The skill required to excel as an IB professional in the AI-first world has expanded from evaluating models and token economics to evaluating physical-infrastructure unit economics: $/kW, MW interconnection queues, fuel pass-through clauses, and multi-decade PPAs.

The Q4 2025 Aligned Data Centers acquisition ($40B by BlackRock GIP, Microsoft, and Nvidia) was not the peak of this trend.

Q1 2026 accelerated this trend by closing with at least 11 separate $1B+ data-center and power-infrastructure transactions in the announced pipeline.

For the Aspiring IB Applicant

The hyperscaler capex cycle has created a category of coverage work that did not exist three years ago: power and grid-infrastructure financing for AI.

Applicants who arrive on day one able to discuss:

• $/MW economics: The cost and profitability math per megawatt of power.

How much does it cost to build or run 1 MW of data center capacity? What’s the revenue per MW? What’s the return on investment? This is the core financial model for AI data centers (which need enormous amounts of electricity).

• Interconnection-queue mechanics

How to get new power plants or data centers connected to the electricity grid.

In the U.S., there are massive delays (often 4+ years) because thousands of projects are waiting in a long queue. Knowing how queues work, how to speed them up, or how to navigate rules is critical.

• Power-purchase-agreement structures

Corporate PPA: A big company (e.g., Microsoft or Google) directly signs a contract with a renewable energy project.

Virtual PPA (VPPA): Companies don’t get the physical electricity, but get the “green credits” and financial benefits for accounting/sustainability goals.

Sleeved Power Purchase Agreement (PPA): is a special type of contract that lets a company (like Microsoft, Google, or an AI data center operator) buy renewable electricity from a far-away wind or solar farm, even if they can’t physically use the power from that location.

In this arrangement, a Renewable Developer ( a wind farm in Texas) generates green electricity and signs a long-term contract to sell it. The Middleman (the “Sleeve”) is usually a utility company or an energy trader (Shell Energy, Goldman Sachs Renewables, or a local utility) that steps in between.

The Buyer (data center in Virginia or Ohio) wants green power, but the wind farm is 1,000 miles away.

By delegating the middle work to the Sleeve, including buying the renewable power from the wind farm, delivering physical electricity to the buyer through the grid, often facing protests and the burden of “virtual” balancing (buying energy shortage arising from renewable and selling energy excess where renewable has high output), and passing on the Renewable Energy Certificates (RECs) or green attributes to the buyer.

Hyperscalers' AI data centers is guaranteed physical clean power 24/7 while complying with regulatory, ESG, and reliability mandates.

• Data-center sale-leaseback math: A company builds a data center, sells it to an investor (BlackRock, infrastructure funds, etc.), and then leases it back. By understanding cap rates, lease terms, returns for the buyer, and accounting impact, the cash could be accounted for as an annual expense item instead of a big asset liability until the ROI is realized from the data center.

Traditional Telecom, Media and Telecom expertise has paved the way for power-and-utilities, infrastructure, and real-assets coverage groups.

MBA electives in energy finance, infrastructure investing, and project finance are equally valuable as building skills to read disclosure documents from recent data-center sale-leasebacks and PPA-backed financings in the public record.

Trend 4: ECM Reawakens with Selectivity, Defense and Convertibles Lead

Equity Capital Markets opened 2026 with the strongest first quarter in five years for US IPO issuance.

PwC reports 22 traditional IPOs raised $9.4 billion through March 31[8].

ICR's Q1 2026 ECM review puts the figure at 21 deals, raising approximately $10 billion[16]. The Q4 2025 IPO thaw has carried forward, but with notable selectivity.

What Worked

• Power infrastructure for AI: The largest US IPO of Q1 was a manufacturer of electrical distribution equipment serving data centers, which traded up more than 8% from pricing

• Defense: EY reports the largest global IPO of Q1 2026 came out of Europe in the defense sector, supported by NATO members moving toward 5% GDP defense spending targets[9]

• Convertibles: Goldman Sachs noted that equity underwriting net revenues were significantly higher YoY, primarily reflecting convertible offerings[2].

With stock markets remaining strong, companies can attract funds with convertibles, which carry a coupon rate that is 2-4% interest rate below comparable debt.

Buyers get the upside of the stock price surge and the downside of a stable 2-4% return on their investments. This risk-minimizing dynamic infuenced Q1 2026 as the quarter saw $31 billion in convertible issuance, with follow-ons at $35 billion and block trades at $7 billion[16].

For investors, the upside if AI-infrastructure and aerospace issuers re-rate at higher rates in H2 2026 is calculated in the issuance.

• Healthcare carve-outs: Notable issuers included a diabetes device carve-out, an equipment-rental platform, and several healthcare and technology companies[8]

What Stalled

• AI application-layer: PwC notes some prospective issuers downsized, postponed, or withdrew transactions as equity volatility increased due to AI's impact on SaaS valuations[8]

• Smaller issuers: Smaller issuers are struggling. According to Renaissance Capital, which tracked 50 IPOs in 2026 through early May, February was the strongest at 16 IPOs, and March was the weakest at only 8 IPOs. Investors are picky as valuations are not attractive for investor participation.

• US vs. global: EY reports US activity declined markedly, with China and Europe (helped by a defense mega-IPO) carrying global IPO value[9]

Implication for the Investment Banker: Flow Book vs. Backlog Book

In Q1 2026, convertibles made up half of all equity-linked issuance.

A successful ECM bankers are long-term strategists who manage a few massive deals over 1–2 years. They spend more time on preparation, waiting for the right market window, and planning backup options or sophisticated financial products.

This long-wait dynamics is called a "backlog environment". In this new dynamic, an IB candidate should have fluency in

(1) convertible-bond structuring

(2) defense-sector industry coverage (NATO members moving toward a 5% GDP defense spending target have already produced the largest global IPO of the quarter and a multi-year listing volume)

(3) dual-track deal management (IPO and sale negotiated in parallel), which EY notes is increasing as issuers want to protect optionality through volatile market windows

(4) the patience and pattern recognition to know when to push a hyper-jumbo issuer (often privately valued above $100 billion) into the market versus when to recommend further private fundraising.

Post-MBA bankers placed in ECM groups in 2026 should expect fewer transactions per year than the 2021 cohort, but each transaction will be substantially larger, more structurally complex, and more closely watched by the rest of the issuance market.

For the Aspiring IB Applicant

ECM in 2026 rewards depth over breadth.

The backlog-book environment means a junior banker works on fewer transactions per year than a 2021 cohort would have, but each transaction is substantially larger and structurally complex.

For applicants, the IPO and convertible markets are becoming more technical again. Just knowing general “ECM” is no longer enough. They should also know the mechanics of going public, including the three timelines: cooling-off periods (15-25 days after filing S-1), comfort letters (auditor's assurance on the accuracy of financials), and syndicate structuring (how the stakeholders - investment banks or the syndicate are organized with breakdown of the fee structure).

Recruiters and hiring managers at top firms want candidates who can talk intelligently about the real mechanics of deals that are happening right now (especially convertibles and IPOs).

Those interested in a career in IB must follow the actual 2026 IPO calendar week by week, read the prospectuses of the largest deals (including S-1 filings), and form a view on why specific issuers chose IPOs versus convertibles versus continued private fundraising. They should also be ready to walk through a convertible deal structure or an IPO timeline in an interview.

ECM groups conduct technical interviews that test for this depth, and the candidates should show awareness of a real issuer's capital-structure choices.

Trend 5: Bespoke Capital Solutions and Private Credit Exposure

The Q4 2025 trend toward bespoke capital solutions accelerated in Q1 2026, with the line between bank lending and private credit functionally erased on every major transaction.

JPMorgan $160 billion Exposure to Private Credit

JPMorgan disclosed in its Q1 2026 earnings call that the firm has $50 billion in private credit exposure as part of $160 billion in total exposure to non-bank lenders[1].

JPMorgan’s exposure to private credit is a layered, multi-year relationship across three channels:

1. Direct loans to private credit funds (warehouse lines, subscription lines, NAV loans).

2. Co-lending with private credit firms on the same deals.

3. Loans originated by JPM that are sold to private credit funds.

CFO Jeremy Barnum called the overall exposure “manageable.”

CEO Jamie Dimon downplayed the systemic risk banks have in private credit. He blamed tight bank regulations for the temporary arbitrage and expects some activity may return to banks once Basel III rules are recalibrated.[1].

Why might private credit revert as Basel III recalibrates?

Private credit grew during the 2018-2025 period in part because Basel III risk-weighted asset rules made certain large corporate loans (particularly leveraged loans, second-lien debt, and concentrated single-name exposures) capital-expensive for banks.

Non-bank lenders, which are not subject to those rules, could underwrite the same loans at a lower required return on capital and still earn a wider spread.

The March 19, 2026, US Basel III re-proposal removes the dual-stack framework and reduces aggregate capital requirements at the largest US banks by approximately 6%[12].

As regulatory capital becomes less binding on bank lending, the relative cost advantage that fueled private credit's growth narrows.

Banks regain the ability to compete head-on for direct-lending mandates, and over time the market should rebalance back toward the regulated banking system. The reversion is not immediate.

Table D - Private Credit vs. Investment Bank

| Loan Type | Time to Close | |

|---|---|---|

| Private Credit (Direct Lending) | 2 – 6 weeks (often 14–45 days) | |

| Bank Syndicated Loan | 8 – 16 weeks (60–120+ days) |

Source: Industry benchmarks from Proskauer Rose (2025), Ares Management [22]

Dimon’s optimism must be tempered with facts. Private credit funds have already raised the committed capital they need to deploy.

Borrowers save as little as 15 days to as long as 106 days in acquiring the fund. Even at 2% higher interest rate, borrowers can remove the ‘complexity’ of the syndicate with single lenders. Private credit loan continues to be the preferred path for distressed companies and any funds looking to infuse funds to stagnant industries.

Hybrid Financing Becomes the Default for Megadeals

The Paramount-WBD financing structure illustrates Q1 2026's standard model. Paramount issued $47 billion in new Class B shares at $16.02 supported by an irrevocable personal guarantee from Larry Ellison of $43.3 billion, alongside committed investment from the Ellison Family and RedBird Capital Partners[10]. This is not a traditional LBO debt package. The financing was a hybrid of equity, family-office capital, and traditional bank financing, structured around a personal guarantee that traditional lending teams could not have arranged five years ago.

Convertibles as the New Mezzanine

Goldman Sachs equity underwriting net revenues were up 45% YoY primarily on convertible offerings[2]. Convertibles now sit between traditional debt and equity in the capital stack of the largest deals, and bankers who can structure them are commanding fee premiums.

Implication for the Investment Banker

The post-MBA banker who shows up to a megadeal pitch in 2026 with only one financing idea (whether bank debt, leveraged loans, or pure equity) will lose the mandate. The expectation is now a layered structure that includes some combination of: senior bank debt, private credit, structured equity (convertibles), and family-office or sovereign-fund equity at the top. Career mobility flows toward bankers who can read across these markets fluently.

In 2026, post-MBA bankers who pitch megadeals with just one financing idea (bank debt, leveraged loans, or pure equity) will likely lose the mandate.

Clients now expect layered financing structures that combine:

• Senior bank debt

• Private credit

• Structured equity (convertibles)

• Family office or sovereign wealth equity at the top

For the Aspiring IB Applicant

Bespoke capital architecture rewards the applicant who refuses to specialize too early.

In 2026, complex deals like the Paramount-WBD financing now use multiple layers of capital — senior bank debt, private credit, structured equity (convertibles), and even large personal guarantees (e.g., Larry Ellison’s $43.3 billion backstop).

A junior banker on that deal had to understand all four layers and how they interact, especially in worst-case scenarios.

Stop following the old advice to specialize early in just one product (M&A, leveraged finance, or ECM). Instead, target platforms that offer cross-product training.

Research and find whether Leveraged Finance, Equity Capital Markets (ECM), and Capital Structuring teams work closely.

Interview junior bankers and find out how they gain expertise across product groups.

For an MBA or a Master's program, choose electives where such a cross-functional perspective is built into the curriculum, either through the professor's background or through the cases they cover.

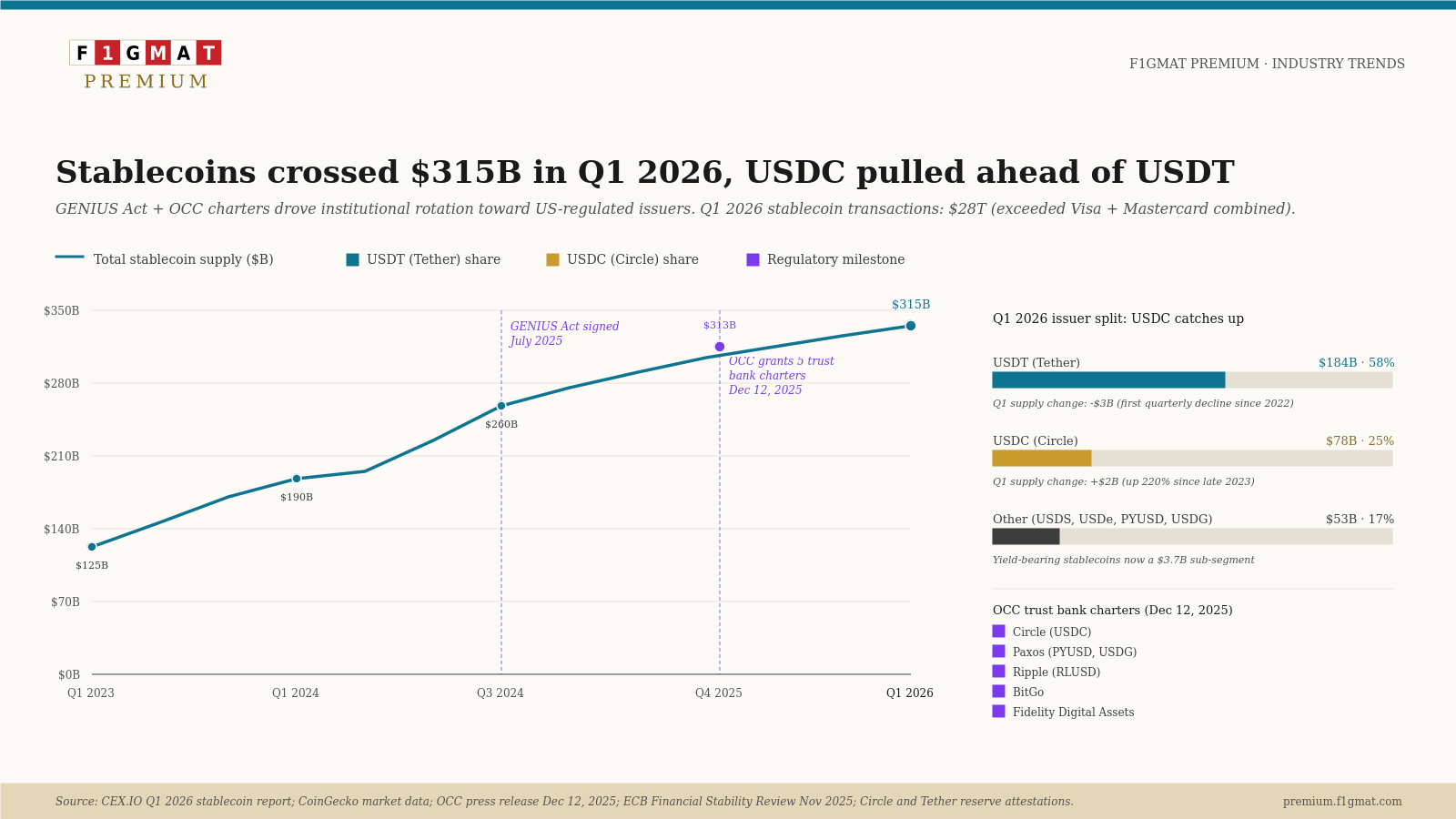

Trend 6: GENIUS Act Implementation Phase Begins as Stablecoins Hit $315B

The GENIUS Act, signed into law on July 18, 2025, moved from policy to operational rollout in Q1 2026.

The OCC, FDIC, and Federal Reserve issued the first wave of implementation actions, and the major stablecoin issuers began operating under the new federal framework.

Bank Charters Granted

In December 2025, the Office of the Comptroller of the Currency (OCC), the U.S. federal regulator for national banks, conditionally granted national trust bank charters to Circle, Paxos, BitGo, Ripple, and Fidelity[13]. This permits a non-bank stablecoin issuer with a national trust charter to directly clear and settle transactions in central bank money, reducing settlement and liquidity risk and simplifying the exchange of stablecoins with bank deposits and cash[13].

OCC Notice of Proposed Rulemaking

The OCC opened a Notice of Proposed Rulemaking on payment stablecoin issuance with a comment window running March 2 to May 1, 2026[13]. The proposal sets reserve requirements, redemption procedures, and capital standards for OCC-supervised stablecoin issuers. Circle filed a public comment letter on May 1, 2026, calling for global stablecoin standards and competitive parity among issuers.

Market Size Reached $315 Billion

Stablecoin supply reached a record $315 billion in Q1 2026, up from $306 billion at the end of November 2025 and $205 billion at the start of 2025[13]. Tether (USDT) holds approximately $188-189 billion (60% of public float), while USDC continues to gain share, having grown 220% over the prior two years.

Tokenized Deposits and the Bank Response

The GENIUS Act prohibits stablecoin issuers from paying interest or yield directly to holders. This has triggered a banker-led response: traditional banks are now developing tokenized deposits (which can pay yield because they are bank liabilities backed by deposit insurance) as a competing product. JPM Coin and similar bank-issued tokenized payment instruments are siphoning capital from non-yield-bearing offshore stablecoins[13].

Implication for the Investment Banker

Stablecoins are reshaping four of the IB stack's core revenue lines simultaneously.

Advisory and capital raising for stablecoin issuers: Circle's July 2025 IPO at a roughly $30 billion valuation, combined with Paxos, Ripple, BitGo, and Fidelity each pursuing trust bank charters, has produced a fee pool that did not exist three years ago.

Beyond IPOs, stablecoin issuers are raising convertible debt, acquiring custodians, and partnering with banks via M&A.

DCM disruption from tokenized issuance: Corporate treasury teams are getting tired of waiting two days for money to move (the old T+2 settlement). They're increasingly shifting their working capital, which they use for paying suppliers, payroll, and cross-border transfers onto stablecoins.

Stablecoins can settle instantly (T+0). Because of this shift, investment bankers who cover big corporates are now helping their clients figure out:

• Which stablecoin is best for them (USDC if they want maximum regulatory compliance and a clean reputation, or JPM Coin if they want smooth integration with traditional banking systems)

• How transparent and safe the reserves behind the stablecoin are

• How to spread their money across different stablecoins so they’re not overly reliant on just one issuer

Treasury management overhauls: Corporate treasury clients in the Trade, logistics, manufacturing, commodity trading are moving from operating cash into stablecoin to improve settlement from T+2 to T+0 and manage the currency volatility of the global supply chain.

Investment bankers are now advising on the choice of stablecoin issuer, from USDC for compliance, JPM Coin for bank-grade integration, and even suggesting a diversification strategy based on the exposure each stablecoin reserves have on the US treasury.

Bankers are also expected to be well-versed in reserve transparency and simulate scenarios where there is a bank run on the stablecoin.

Custody and prime brokerage Partnerships: Banks are now acquiring or partnering with Digital-asset custodians (Coinbase Custody, Fireblocks, Anchorage, BitGo) to safely store cryptocurrencies and tokenized assets because once a client stores assets with the bank (custody), it opens the door to cross-selling higher-margin services like margin lending, lending out tokens or stocks, or trading options, swaps on tokenized assets.

For the post-MBA banker, stablecoin literacy sits alongside Basel III capital and antitrust as one of the three core regulatory frameworks a banker must navigate to advise a major client in 2026.

MBA Curriculum Implications

MBA programs targeting investment-banking placement should consider adding the following courses or course modules to remain credible for IB recruiters in this new world: Tokenized Capital Markets, Stablecoin Reserve and Treasury Management, Digital Asset Regulatory Frameworks, Bespoke Capital Architecture, Programmable Payments and Cross-Border Infrastructure, Bespoke Capital Architecture, and Geopolitical Risk for Capital Markets.

Programs that integrate even three or four of these 7 modules will be substantially more attractive to IB recruiters at Tier-1 firms by 2027-2028. By then, the GENIUS Act framework will be fully operational and tokenized-issuance volumes will no longer be niche strategy.

Trend 7: Basel III Revision, US Banking Capital Re-proposed

On March 19, 2026, the Federal Reserve Board, the Office of the Comptroller of the Currency(OCC), and the Federal Deposit Insurance Corporation jointly issued three proposals that comprehensively overhaul the existing US bank capital framework, implementing the Basel Committee's 2017 endgame revisions[12].

The Federal Reserve voted 6-1 to advance the proposals (Governor Michael Barr was the sole dissenting vote), with comments due by June 18, 2026[12].

What Changed Versus the 2023 Proposal

The 2023 proposals would have substantially increased capital requirements; the 2026 re-proposal would reduce overall capital requirements at the largest US banks by approximately 6%[12].

The proposal removes the dual-stack framework (where banks calculated capital using both standardized and internal models) and emphasizes a simpler structure built on standardized methodologies for credit and operational risk.

G-SIB Surcharge Recalibration

The Federal Reserve separately issued a proposal to modify the coefficients used to calculate the G-SIB capital surcharge and to introduce automatic annual updates that adjust for economic growth and inflation[12]. This addresses a long-standing complaint from the largest US banks that the original surcharge had a cliff effect.

Cross-Jurisdictional Status

In the UK, the Prudential Regulation Authority finalized Basel 3.1 in early 2026 for January 1, 2027 implementation, and deferred the Fundamental Review of the Trading Book Internal Model Approach to January 1, 2028[12]. In the EU, the European Commission postponed FRTB implementation first to January 1, 2026 and then to January 1, 2027. The result is that all three major Basel jurisdictions are now aligned on a 2027-2028 implementation horizon.

Impact of Risk to the Entire Financial System

The systemic-risk question is the most contested element of the March 19, 2026 re-proposal.

The case that systemic risk increases

Critics of the re-proposal points that the proposals reduce overall capital requirements at the largest US banks by approximately 6%[12]. A smaller capital cushion mechanically means less ability to absorb losses in a crisis, holding everything else constant.

Removing the dual-stack framework eliminates a check on internal-model gaming (under the 2023 proposal, banks would have been required to compute capital under both standardized and internal models and use the higher of the two; under the 2026 re-proposal, that constraint is gone).

Governor Michael Barr, the lone dissenting Fed vote, argued that the re-proposal weakens the capital regime at a moment when private-credit growth, AI-infrastructure leverage, and stablecoin's integration with the traditional financial system are all introducing new risk vectors that were not visible when Basel III was originally designed.

The case that systemic risk decreases

Supporters argue that the 2023 proposal's higher capital requirements would have pushed lending out of the regulated banking system and into private credit and other non-bank channels, exactly what happened in the 2018-2025 cycle.

Lending that migrates from banks to less-transparent, less-supervised entities concentrates in a sector with weaker liquidity backstops, no Fed discount window access, and limited public disclosure.

By keeping bank lending economic, the re-proposal arguably keeps risk inside the institutions where regulators can see it.

Aggregate capital in the US banking system also remains substantially higher than pre-2008 levels, so a 6% reduction off a much-higher base is a different question than a 6% reduction off the 2007 baseline[12].

The G-SIB surcharge automatic-update mechanism (which adjusts coefficients annually for economic growth and inflation) introduces a dynamic countercyclical element that the original framework lacked.

Net assessment. The bet only works if :

(1) Basel III recalibration actually narrows the private-credit arbitrage (Trend 5)

(2) Banks deploy the freed-up capital into productive lending and not on buybacks, and

(3) The next stress event arrives slowly enough for the dynamic G-SIB surcharge to recalibrate before losses crystallize.

What are Globally Systemically Important Banks (G-SIBs)

The Adjustable capital buffer (surcharge) that Globally Systemically Important Banks (G-SIBs) must hold above standard minimum capital requirements. This surcharge is not fixed. It varies every year. It is designed to make "too-big-to-fail" banks more resilient by forcing them to internalize some of the systemic costs their potential failure would impose on the broader financial system.

The June 18, 2026 comment deadline will reveal whether market participants accept this framing.

Implication for the Investment Banker

The re-proposal is a deregulatory pivot.

It expands balance-sheet capacity at the largest US banks at the same moment that megadeal financing demand is peaking.

Goldman Sachs, JPMorgan, and Morgan Stanley enter Q2 2026 with the prospect of less binding capital constraints just as the M&A backlog converts to closed deals.

For post-MBA bankers, this means the regulatory capital desks (often viewed as middle-office) are now generating front-office quality questions: how should the bank price acquisition financing under the new rules, where should leveraged finance be reweighted, and what new lending verticals become economic?

For the Aspiring IB Applicant

Regulatory capital is a topic most IB applicants ignore.

The March 19, 2026, Basel III re-proposal runs hundreds of pages and most candidates will not read it.

Even basic fluency - knowing what risk-weighted assets are, what the dual-stack framework was, and why the 6% reduction in capital requirements matters puts a candidate well ahead of peers and signals that the candidate reads beyond the standard interview-prep guides.

Recruiters at Goldman, JPMorgan, and Morgan Stanley have all flagged regulatory literacy as a differentiator at the associate level over the past two recruiting cycles.

Key Takeaways

Three Cross-Cutting Themes

1. Concentration at the top. Whether in M&A (megadeals), ECM (large IPOs and convertible issuers), or hyperscaler capex (Big Five at $660-725 billion combined), the Q1 2026 market rewards size.

Smaller transactions and smaller issuers are stuck on the wrong side of the K curve.

2. Regulatory rebalancing. Three regulatory frameworks moved into operational mode simultaneously: the GENIUS Act for stablecoins (OCC trust-bank charters granted, NPRM comment period closed May 1), Basel III re-proposed for US bank capital (March 19 release, June 18 comment deadline), and FRTB now aligned across the US, UK, and EU with a 2027-2028 implementation horizon.

Bankers must hold all three frameworks in their head to advise a serious client in 2026.

3. Capital-stack creativity. The standard 2026 megadeal involves: senior debt, private credit, convertibles, and family-office or sovereign-fund equity. The Paramount-WBD financing combined all four with a $43.3 billion personal guarantee from Larry Ellison. Cross-product fluency is the differentiator.

For the Banker in Seat

Based on the Q1 2026 investment banking trends and the changes in the regulatory and investment environment, three profiles will thrive in the next 2-3 years.

First, advisory bankers are consolidating verticals like AI infrastructure, media, biopharma, and energy. Second, ECM bankers are fluent in convertibles and dual-track processes, and third, capital-markets bankers who can structure across debt, equity, and hybrid instruments.

What used to be a less glamorous role, the regulatory capital advisory role, considered a middle-office speciality will gain more value.

Digital asset literacy will expand from a could-have skill to a mandatory foundation for IB roles.

The advisory groups at Tier-1 firms entered Q2 2026 with the strongest deal flow and the clearest career paths since 2021.

The leveraged-finance desks lag, since the leveraged loan market has not yet caught up with strategic M&A.

For the Applicant Planning to Enter IB

1. Target advisory and ECM groups at Tier-1 firms; the revenue growth and the hiring concentration both sit there, while DCM and leveraged finance are flat to soft.

2. Since the megadeal fee pool concentrates in the same four to five sectors (AI, Pharma, Energy, and Media - recent cycles) and coverage groups handling those mandates carry the strongest deal flow per junior hire, prioritizing firms serving these 4 to 5 sectors is a better strategy.

What to Watch Into Q2 2026

• Basel III Revision Deadline: When the comment period closes on June 18, 2026, we will understand whether the fight to keep the capital reserve to 6% holds. Banks, as expected, want this new ruling. The Fed and the FDIC are not in favor of the new rule.

• Q2 IPO Pipeline: The $100B-plus IPO from Stripe, SpaceX, and Databricks has been in talks for a long time. Q2 2026 will be the test of these favorite brands.

• Leveraged Finance Recovery: If Q2 leverage loan revenue at the big banks runs on loss, the M&A wave will no longer rescue these banks, and we might witness a reversal in fortune.

• OCC Trust Charters: Circle, Paxos, BitGo, Ripple, and Fidelity have already received the banking charter. The next 5 charters will determine whether the GENIUS Act is working to deregulate the banking industry.

• Power-Grid Constraints: Northern Virginia and ERCOT already said no more to power grids. PJM-Ohio, Arizona, and Georgia are the next focal points. The Capex spending is no match for the protests. If history is a lesson, Greed beats socialism.

References

- JPMorgan Chase Q1 2026 Earnings Press Release (Form 8-K) ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Goldman Sachs Group Q1 2026 Earnings Results (SEC Form 8-K) ↩ ↩ ↩ ↩ ↩

- Morgan Stanley First Quarter 2026 Earnings Results (April 15, 2026) ↩ ↩ ↩ ↩

- Citigroup Q1 2026 Form 10-Q (period ended March 31, 2026) ↩ ↩ ↩ ↩

- Wells Fargo Q1 2026 Earnings Presentation (Form 8-K Exhibit 99.3) ↩ ↩ ↩ ↩

- PitchBook Global M&A Report Q1 2026 (via Fintech News CH summary) ↩ ↩

- S&P Global Market Intelligence: Global M&A by the Numbers, Q1 2026 ↩ ↩ ↩

- PwC US Capital Markets Watch Q1 2026 ↩ ↩ ↩

- EY Global IPO Trends Q1 2026 ↩ ↩

- Paramount-Warner Bros. Discovery Definitive Merger Agreement (WBD Form 8-K filed February 27, 2026) ↩ ↩ ↩

- SpaceX-xAI acquisition (combined valuation $1.25T; xAI at $250B) ↩

- US Basel III Endgame Re-Proposal of March 19, 2026 (Bloomberg Professional Services analysis) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Brookings: Next Steps for GENIUS Payment Stablecoins (March 6, 2026) ↩ ↩ ↩ ↩ ↩

- Hyperscaler Capex 2026 Estimates ($660-690B Big Five guidance, Microsoft Azure power constraints, Q1 2026 capex update) ↩ ↩ ↩

- Wall Street Horizon: Megadeal Volume Up 57% YoY (March 7, 2026) ↩

- ICR Q1 2026 Equity Capital Markets Review ↩ ↩

- Inside Elon Musk’s $1.25 Trillion AI and Space Megamerger ↩ ↩

- Centerview Partners & RedBird Advisors Win $111B Paramount-Warner Bros. Deal ↩

- Abbott to acquire Exact Sciences, a leader in large and fast-growing cancer screening and precision oncology diagnostics segments ↩

- Wells Fargo Agrees to Pay $3 Billion to Resolve Criminal and Civil Investigations into Sales Practices Involving the Opening of Millions of Accounts without Customer Authorization ↩

- Federal Reserve Board announces termination of enforcement action with Wells Fargo ↩

- Overview and comparison of the broadly syndicated loan and private credit markets | Private Debt Dominance ↩

- BoFA Revenue ↩ ↩ ↩ ↩ ↩ ↩